This project employs behavioural science tools to ask why customers do not engage with consent artefacts and how that can be reversed. The specific use case we took up for the study is digital lending and (therefore) the consent screens presented by RBI-licensed account aggregators. We discover that the macro- context of a borrowing journey is characterised among low- income borrowers by financial desperation, the urgency of time and an acute awareness

that they may be denied formal credit for no proper reason. This macro-context shapes individuals’ micro-decision of consent, immediately placing them on the defensive. Furthermore, the shrink-wrap design of consent artefacts offers little scope for negotiation or challenge, affording customers little real choice or control. As a consequence, customers feel resigned to passively comply.

that they may be denied formal credit for no proper reason. This macro-context shapes individuals’ micro-decision of consent, immediately placing them on the defensive. Furthermore, the shrink-wrap design of consent artefacts offers little scope for negotiation or challenge, affording customers little real choice or control. As a consequence, customers feel resigned to passively comply.

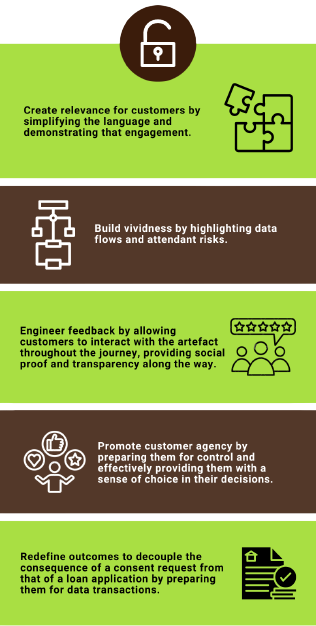

A customer-friendly consent artefact would assuage the negative emotions triggered by prospects of borrowing, empower customers during the process and be easy for the customer to comprehend. For this to happen, the consent form should have the elements as shown in Illustration 1.4

At the time of this publication, the team is translating these principles into specific design recommendations which will be piloted with customers of a lender and account aggregator to test their effectiveness.

Read all our writings under Customer’s Consent here.

A law would improve personal data protection practices in two ways. First, it would bring under its fold those financial intermediaries that may reside outside of the perimeter of financial sector regulators. Second, it would set a minimum baseline for personal data protection even where financial sector regulators may not have provided active guidance. For these reasons, engagement with the Bill is critical, and we note the action items in Illustration 1.5 for strengthening its customer protection impact.

Read all our writings under Data Protection here.