Guest post by Jaya Umadikar (RTBI), Prerit Srivastava (Qarth) & Gaurav Raina (IITM)

Since its introduction in 2010, IMPS based mobile banking transactions have been growing month on month reaching 3.5 Million monthly transactions in May 2014. However even with high penetration of mobile phones, mobile financial services haven’t seen a massive adoption among the rural population.

To explore the challenges in adoption of Mobile Financial Services (MFS) among the rural population, a pilot was conducted by Pudhuaaru KGFS & Qarth Technologies (an IMPS based mobile payment startup). The objective of the pilot was to understand the challenges in adoption of MFS, getting Pudhuaaru KGFS customers to make loan repayments via a customized banking application and understanding other use cases for MFS among the rural population.

Neivasal village in Thanjavur district, Tamil Nadu was chosen as the test bed for conducting the pilot. While the majority of Pudhuaaru KGFS customers in Neivasal had bank accounts, most of them were in a deactivated state due to non-usage. The nearest bank branch was 5km away, and the nearest ATM was 7km away from the village. All repayments were done via cash, either by visiting the nearest Pudhuaaru KGFS branch on the due date, or by making the payment to a local Pudhuaaru KGFS collection agent.

To ease the adoption, Pudhuaaru KGFS in partnership with Qarth developed a customized, and user-friendly, application for mobile banking for Java and Android phones. The application enabled the customers to make their loan repayments directly from their bank accounts to Pudhuaaru KGFS, without the need to travel to an Pudhuaaru KGFS branch. The application could be used 24×7, and could transact over the SMS channel. There was no requirement for GPRS/3G for making transactions. A key additional benefit of the application was the ability to provide mobile and DTH recharge functionality. With this facility, customers could earn 2% commission on each recharge provided and thus provided an additional revenue stream. This immediately provided the much-needed incentive for customers to keep a minimum balance in their bank accounts, and to adopt a mobile financial services platform.

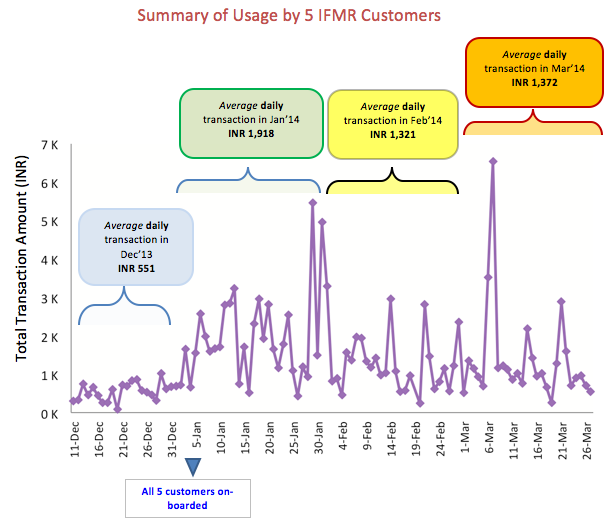

The pilot was started off with 5 Pudhuaaru KGFS customers being enrolled for mobile banking with their nearest bank. The customers were small shop owners – two general merchants, a tailor, a fertilizer shop and a brick maker with an average loan installment ranging from INR 700 (weekly payment) to 5,000 (monthly payment). The results were extremely encouraging: within the first 100 days, the customers conducted 2,982 IMPS transactions over a net sum of INR 1.43 Lakhs.

There success in adoption points to range of potential benefits for Pudhuaaru KGFS, the customers and Banks. By implementing such a solution each Pudhuaaru KGFS branch can serve a larger area, as proximity to customers is not required while saving on collection agent costs. Customers opting for loan repayment via mobile also save on travel costs while avoiding being absent from business. It also allows the customers to switch to faster loan repayment cycle leading to reduction in interest rates. The supporting bank also benefits by having more number of active accounts with higher average account balance.

The pilot also provided lessons for simplifying and scaling the IMPS platform for payments. We collected our recommendations in terms of technology enhancements, enrollment processes, awareness and pricing.

Technology enhancements: Currently IMPS transactions are carried over an un-encrypted SMS channel. This has two drawbacks: first, is security, and second, due to lack of security the transaction limits are capped. Given that India has such a large SMS consumer base, it would be important to have standards for encrypting SMS based transactions. Given the success of the customized application, standards for the development of multi-bank applications by third parties should be expedited and encouraged.

Enrollment process: Most banks require multiple visits by customers to the branch to get registered for mobile banking and to get their MMID & MPIN. Such processes should be simplified, and ideally standardized, across all banks. To this end, the use of alternate channels for registration and enrollment like interoperable ATMs should be facilitated.

Awareness: We found lack of awareness not only among the customers, but also among the bank staff. Advertising on popular media can help customers, but the banks should also initiate training and awareness programs within themselves.

Pricing IMPS payments: There are two ways to help customers in this regard. First is by charging customers, per transaction, only after they cross a monthly transaction limit. After this limit, the charges should be reasonable so that they encourage even low-value transactions. Secondly, the cost of the SMS can be reduced by the introduction of toll free numbers for SMS banking.

The above challenges have also been recognized in the Report of the Technical Committee on Mobile Banking released by the RBI on February 7th 2014. However, the pilot provides some on the ground experience on both the potential and some of the bottlenecks for mobile financial services. Overall the pilot was able to provide a sense of the tremendous demand and untapped potential for MFS among rural customers. With over 900 million mobile phone subscribers in India, mobile-based solutions can bring about a sea change in the way rural population avails various financial services and play an active part in the growth of financial ecosystem of the country.