The Committee on Comprehensive Financial Services for Small Businesses and Low Income Households (CCFS) envisions the following:

By January 1, 2016 each Indian resident, above the age of 18 years, would have an individual, full-service, safe, and secure electronic bank account.

By January 1, 2016, the number and distribution of electronic payment access points would be such that every single resident would be within a fifteen minute walking distance from such a point anywhere in the country. Each such point would allow residents to deposit and withdraw cash to and from their bank accounts and transfer balances from one bank account to another, in a secure environment, for both very small and very large amounts, and pay ― reasonable charges for all of these services. At least one of the deposit products accessible to every resident through the payment access points would offer a positive real rate of return over the consumer price index.

India has a rich and diverse payments infrastructure in place already and a number of measures have been taken by the RBI to activate this infrastructure. However, despite all the effort, while 89% of all urban areas have a full service payment access point within a fifteen minute walking distance from households, only a mere 3% of all rural areas do.

Strategic Direction

In order to address this gap, the CCFS recommends the following strategic directions.

- Shift towards electronic money – The Committee recommends a regulatory shift from the restricted use of electronic money, especially by non-banks, towards a cash-less society. While progress can be made by cross-subsidisation and the use of more efficient non-branch but cash-based channels such as BCs and ATMs, the financial inclusion and efficiency gains associated with the wide-spread, even ubiquitous use of electronic money are likely to be very high to individuals, businesses, and the Government.

- Enhance the distribution of payment points – In order to achieve the vision outlined above, more than 30 lakh payment points are required with a much greater proliferation in rural areas, which are able to provide very small value transactions efficiently and in a secure manner. Banks along with BCs have proven effective and efficient in high density urban areas offering credit and savings products offered together. Credit, however, is a significantly more specialised activity with important risk and cost considerations, and something that customers need to access less frequently. Payments, however, is a universal need for all citizens and the infrastructure for payments needs to proliferate independent of credit. Independent non-bank players have an important role to play with their wide customer bases and deep penetration in low-revenue rural areas by leveraging other “adjacencies” such as retailing and mobile telephony that have even higher risk-adjusted margins than credit.

The CCFS also recommends that other critical enablers be put in place such as the existence of a universal electronic bank account (UEBA), resolution of Know-Your-Customer (KYC) issues, suitable authentication strategies, and smooth inter-operability across channels.

Universal Electronic Bank Account (UEBA)

The CCFS recommends the creation of a process wherein an electronic bank account is automatically assigned to every citizen at the point that she gets an acceptable identity number such as Aadhaar. Bank accounts provide direct access to services such as receiving DBT payments electronically and a gateway to all other financial services including those supervised by other regulators. Opening bank accounts in field settings for individuals is often difficult and expensive, but not having one is equivalent of being shut out of the entire financial system.

The CCFS recommends that the UIDAI initiate an instruction to open a bank account upon the issuance of an Aadhaar number to individuals over the age of 18. Customers would be able to choose from a list of banks that have indicated their willingness to open such an account with the understanding that banks would charge no account opening fee but be free to charge for all transactions, including balance enquiry for adequate compensation. As a representation of demand, the UIDAI has already indicated that there are over 24 crore individuals that have an Aadhaar number and wish to have a bank account. In addition, the CCFS recommends RBI to mandate that no bank can refuse to open an account for a customer who has adequate KYC which specifically includes Aadhaar. With Aadhaar as the central piece of the process and given its rapid pace of enrolment, the deadline of January 1st, 2016, while ambitious, is not infeasible.

KYC Guidelines

Current Know-Your-Customer (KYC) guidelines from the RBI are very different from those of other regulators and require that in addition to a proof of identity the individual provide documented proof of her current address. While proof of identity can be obtained by the individual from local authorities at the place at which they were born, proof of local address is much harder to obtain and is perhaps now the most significant barrier to opening a bank account for many individuals in urban and rural environments.

The Committee believes that a superior approach would be to insist on a strong proof of identity like Aadhaar irrespective of current address and account balance, and to require financial institutions to internally develop their own risk based processes linked to transactions monitoring and usage patterns. This approach, in the Committee’s view, particularly with the advent of Aadhaar, will make it much easier for multiple channels of financial access to become fully engaged in the task of ensuring universal access to payments and savings services. It will also serve to converge the KYC requirements of multiple financial and non-financial regulators making the process of customer acquisition and customer migration from one service provider to another much easier and at lower costs.

Customer Authentication

As the payments network is sought to be scaled up, customer identification and authentication becomes very important so that repudiation and fraud risks are minimised, with Aadhaar being the crucial piece of underlying infrastructure. While anticipating that over time the cost of biometric authentication devices will fall sharply and BBNL will expand the reach of its NOFN project, the Committee recommends that authentication for the purpose of transactions happen in either of the three ways:

- Fingerprint in combination with the Aadhaar number or the bank account number (Token-less authentication)

- One-time Password (OTP) in combination with the Aadhaar number or the bank account number (Token-less authentication)

- PIN in combination with the Aadhaar number or the bank account number (Token authentication)

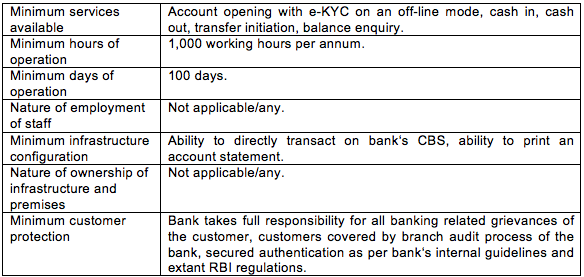

Rural Branching Mandate

While the financial inclusion gap may be filled quickly and automatically by the strong emphasis on achieving priority sector outcomes by building specialisations and the inclusion of newer business models and participants, the complete removal of the 25 per cent rural branching requirement for unbanked rural centres (Tier 5 and Tier 6) might be premature. The CCFS therefore proposes to clarify that under the existing rural branching mandate, a qualifying branch be understood to have the following features:

The Committee also recommends that the policy of mandatory rural branching be reviewed regularly and be phased out once the goals specified in the vision statement for payments services and deposit products have been achieved.

A subsequent post will highlight the recommendations around various bank and non-bank channels that will serve to deliver a ubiquitous payments network and universal access to savings.