BNPL is growing rapidly in India, and it is projected to grow ten-fold in the next four years (Live Mint, 2022). It holds the promise of bringing thin-filed customers in the fold of formal credit (Mukherjee, 2021). However, its marketing as a deferred payments product, the ambiguity around its implications for customers’ credit scores, and the lack of transparency about costs to the customer raise crucial customer protection concerns (Financial Conduct Authority, 2021).

This post first explores the back-end process of BNPL lending. It then unpacks the BNPL revenue model, detailing various costs for merchants, regulated entities (REs), and customers, and concludes with a discussion on emerging concerns for customer protection.

What is BNPL lending and how does it work?

BNPL is a form of short-term credit financing that allows customers to defer payments for purchases (Financial Conduct Authority, 2022). Typically, BNPL providers step in to pay merchants for any purchases made by the customer, while the customer repays the BNPL provider later. Repayments could be structured as one instalment (usually without interest) or through equated monthly instalments (EMIs) (which may carry interest). The credit limit and the repayment tenure vary across BNPL providers (Bhargav, Shetty, & Nayar, n.d.; Narayanan, 2022; Khatri, 2020).

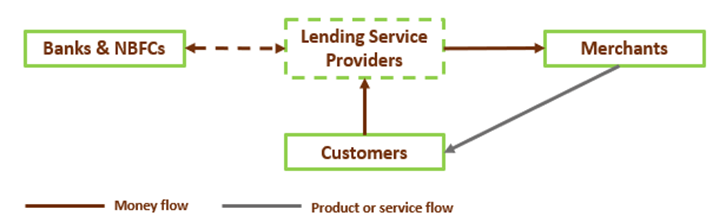

The value chain of BNPL typically comprises four players (Figure 1):

-

RBI-regulated entities (REs) like banks and NBFCs that offer credit lines to customers directly or through loan service providers (LSPs).[2]

-

Unregulated LSPs like BNPL mobile application providers that partner with REs and provide customers a front-end for accessing credit.

-

Merchants that provide goods and services.

-

Customers who borrow BNPL credit (Saxena, 2021; Iyer, 2021).

Figure 1: How BNPL lending works

BNPL lending is offered through two major channels –

-

Mobile application or web-based lending : In this channel, credit is usually offered through mobile applications and websites of BNPL providers. These providers are also embedded in web and mobile applications of merchants say e-commerce, ride hailing etc. Providers such as PayTM Postpaid, Simpl and ZestMoney make use of this channel.

-

Card -based lending: In this channel, customers access BNPL credit through a prepaid card backed by a credit line from an RE. Providers such as Slice, Uni and Dhani offer this product (Bose, 2022; Manikandan, 2022).

What is the BNPL lending business model?

The major sources of revenue for BNPL providers include:

-

Commissions from REs: LSPs charge REs a commission when they originate BNPL credit for them.

-

Commissions from merchants: BNPL providers charge merchants a percentage of their transaction amount with customers as fees. These transaction fees are among the main sources of revenue for BNPL providers (Khatri, 2020; Kumar N. , 2021).

-

Charges on customers: The charges that customers may pay the BNPL provider can be broadly divided into –

-

Charges at the time of availing the loan,

which include subscription fees, activation fees, electronic clearing service (ECS) mandate charges, and BNPL card-related charges. For instance, some providers charge subscription fees that gives customers a zero-interest rate credit line (Ramanathan A. , 2021). Others charge a one-time activation fee for activating the credit line (Alawadhi, 2021). Providers that offer card based BNPL credit charge customers for a variety of services, including card replacement, cash withdrawal, and charge slip retrieval (Slice, 2021). Providers may also charge interest and processing fees if customers opt for a longer repayment tenure through EMI (Amazon Pay Later, n.d.).

-

Post-default charges,

which include late fees, prepayment charges, ECS bounce penalties, and interest. Late fees are levied when customers do not make timely repayments (Dubey, 2021; Kumar N. , 2021). The quantum can differ across providers based on the amount due from the customer. Providers may also charge interest on the late fees for every day of default (Makwana, 2021). Some providers levy prepayment charges if customers pay their dues before the scheduled period (Kaushal, 2022). Providers can also charge interest on the amounts due if the customer defaults on their repayment (Kumar N. , 2021).

-

Therefore, even when BNPL is marketed as a zero-interest credit product (Singh, 2022), it can impose different kinds of costs on customers.

What are the concerns arising for customer protection?

Despite its potential to increase access to credit, BNPL lending can pose pressing concerns for customer protection. In this section we lay out some of these concerns emerging from the use of BNPL products. Some of these concerns may not be unique to BNPL lending. However, they are amplified by the convenient and hassle-free processes of accessing credit that are embedded in the purchase of the product. These processes can often make customers overlook the debt they will incur by using BNPL credit:

-

Risk of misconduct:

BNPL lending is marketed under different labels, but they are mostly embedded as a payment option, which can be misleading. The debt obligations of customers, that come from using BNPL credit, are usually detailed in lengthy and complicated disclosures. Customers are likely to ignore these disclosures or discount their obligations to obtain credit quickly (Busara Center for Behavioral Economics, 2021). Experiences from more mature BNPL markets, like the United Kingdom, suggest that customers are often unaware that they are purchasing credit that must be repaid (Financial Conduct Authority, 2021; Jones, 2022). In India, there have been instances of a BNPL provider sanctioning a large line of credit in the customers’ name without the customers’ knowledge (Ramanathan & Kalyanaraman, 2022). There are also concerns of aggressive debt collection practices by agents against customers (Pinapala, 2021). Insights from complaints on Twitter against three BNPL providers[3] indicated that customers who are overdue for small amounts for a short period of time, and even customers who have repaid dues, sometimes face issues from collection agents. -

Heightened risk of unsuitable debt due to misconduct:

As discussed above, the credit-like features of BNPL – interest on late payments, obligations to repay – are not sufficiently emphasised at the time of offering the product to the customer. This is known to influence customers to borrow more than they can afford (Busara Center for Behavioral Economics, 2021; MicroSave Consulting, 2019; Johnen, Parlasca, & Musshoff, 2021). Customers may pile up debt which they may either find distressing to repay or may default (Pinapala, 2021), incurring high costs in fines and penalties (Kumar N. , 2021). For instance, customer experiences in the United Kingdom suggest that more than 40% of BNPL customers struggled with repayments. In Germany, BNPL customers often lost track of their BNPL debts (BEUC, 2022). -

High and hidden costs:

One other concern is that the costs of BNPL could be high and often not clear upfront. For instance, a customer may have to pay up to Rs 200 in penalties and late payment fees if they do not repay a transaction worth Rs 250 within 80 days (Ola, 2021). Late payment fees can amount to a high proportion of the transaction size. -

Data protection concerns:

Like other digital financial service providers, BNPL providers process extensive amounts of personal data collected directly from the customer (Bank Bazaar, n.d.). Other kinds of data are indirectly accessed through third parties for making risk assessments, including credit information, customers’ transaction history, social media data, and educational qualifications (Kaushal & Adhikari, 2022). Consequently, this can make customers vulnerable to a variety of data protection risks. While these risks are not unique to BNPL lending, they may be more relevant in its context. Given that BNPL providers typically do not seek collateral against small ticket loans, they rely on technology to identify risky borrowers. These algorithms and analytics parse through transactions to generate rich credit-behaviour profiles (Ghosh, 2017). -

Risks to credit scores:

There are three major risks to credit scores that can surface –-

Inadequate disclosures

about BNPL lending can result in customers being unaware of how using BNPL lending can affect their credit scores. In many cases, customers may not know they are purchasing a credit product when they use BNPL lending. This could automatically mask the possibility that BNPL lending can affect customers’ credit scores. At the same time, it is unclear if BNPL providers report customers’ BNPL lending transactions to credit bureaus. Our review of the terms and conditions of ten prominent BNPL providers in India suggests that most of them collect credit information.[4] However, they do not clarify if they also report to the credit bureaus. There is mixed evidence that using BNPL lending, or of defaulting on repayments, can affect credit scores (Kumar N. , 2021). -

Adverse effect on prospective customers’ credit scores.

Customers may often not realise that BNPL providers can query bureausfor their credit information. This can cause customers’ creditworthiness to decrease, even if their request for credit is rejected (Kumar A. , 2019; Singh, 2022; Ramanathan & Kalyanaraman, 2022). This could be unfair to customers, especially when information disclosures do not conspicuously mention querying their credit bureau records, and that it may not be immediately apparent to customers that a query of their records could adversely affect their credit score. -

The lack of formal standards for credit bureaus for recording BNPL loans results in providers either not reporting BNPL transactions or reporting them inaccurately

(Anand & Phartiyal, 2021; Carrns, 2022; Ramanathan & Kalyanaraman, 2022). Currently, BNPL providers report the overall credit amount offered to a customer through a line of credit. They do not report the credit amount disbursed i.e.; the amount utilised by the customer. Therefore, this credit line (even if unutilised) appears as a ‘loan’ on the customer’s credit report until the customer deactivates their account. It appears that leaving the credit line unutilised could also lower credit score (Singh, 2022). However, credit bureaus have started developing standards for reporting BNPL transactions (Carrns, 2022), which could help make credit reporting processes more accurate.

-

-

Inadequate grievance redress:

Our review of the terms and conditions of ten prominent BNPL providers suggests that grievance redress policies can be difficult for customers to find. The policies are usually embedded deep within websites or within fine text. This puts the onus of finding and understanding a BNPL provider’s redress policy on the customer. Some providers direct customers to contact the RE that financed the BNPL credit. However, customers may face sharp information asymmetries in understanding such a direction. Customers may rarely understand if they are engaging with an LSP or with an RE, which makes it difficult to approach the correct forum for redress (Chivukula, 2021). Further, the terms & conditions may not always explicitly mention the BNPL provider’s partnership with an RE. This challenge could foreclose redress entirely for customers. Customers may also have to navigate a cumbersome redress process (Wang, 2021).

BNPL lending holds potential to improving access to credit for those who do not qualify for credit cards. However, BNPL lending needs to be brought under the fold of customer protection frameworks for this access to realise better customer outcomes.

References

Alawadhi, N. (2021, October 06). MobiKwik Bullish on Core Busines, Buy-Now-Pay-Later launched in May 2019. Business Standard. Retrieved from https://www.business-standard.com/article/companies/mobikwik-bullish-on-core-business-buy-now-pay-later-launched-in-may-2019-121100601219_1.html

Amazon Pay Later. (n.d.). Retrieved from https://www.amazon.in/gp/help/customer/display.html?nodeId=GJ626ASQQ6PD2KZY

Anand, N., & Phartiyal, S. (2021, November 8). Buy now, pay alter business set to surge over ten-fold in India. Retrieved from Mint: https://www.livemint.com/industry/banking/buy-now-pay-later-business-set-to-surge-over-ten-fold-in-india-11636370182746.html

Bank Bazaar. (n.d.). Buy Now Pay Later (BNPL). Retrieved from https://www.bankbazaar.com/personal-loan/buy-now-pay-later.html

BEUC. (2022). Factsheet – Buy Now Pay Later products. Retrieved from BEUC: https://www.beuc.eu/publications/beuc-x-2022-017_buy_now_pay_later_products.pdf

Bhargav, A., Shetty, K., & Nayar, V. (n.d.). Regulating buy-now-pay-later Fintechs. International Bar Association. Retrieved from https://www.ibanet.org/article/34FFE3BA-3990-4169-8194-3CFDCCB17006

Bose, S. (2022, January 25). Fintechs issue BNPL cards to push usage at offline stores. Financial Express. Retrieved from https://www.financialexpress.com/industry/fintechs-issue-bnpl-cards-to-push-usage-at-offline-stores/2414758/

Busara Center for Behavioral Economics. (2021). The Digital Credit Landscape: Focus on Kenya, Nigeria and India. Retrieved from Busara Center for Behavioral Economics: https://busaracenter.org/report-pdf/Gates-Digital-Credit-Report.pdf

Carrns, A. (2022, January 2). Buy now, pay later loans may soon play bigger role in credit scores. Retrieved from The Economic Times Markets: https://economictimes.indiatimes.com/markets/stocks/news/buy-now-pay-later-loans-may-soon-play-bigger-role-in-credit-scores/articleshow/88644363.cms?from=mdr

Chivukula, C. (2021, February 18). Consumer Grievance Redress in Financial Disputes in India. Retrieved from Dvara Research: https://dvararesearch.com/2021/02/18/consumer-grievance-redress-in-financial-disputes-in-india/

Dubey, N. (2021, September 10). What you should know while shopping with BNPL. Retrieved from Mint: https://www.livemint.com/money/personal-finance/what-you-should-know-while-shopping-with-bnpl-11631215650470.html

Financial Conduct Authority. (2021, February 2). The Woolard Review – A review of change and innovation in the unsecured credit market. Retrieved from Financial Conduct Authority: https://www.fca.org.uk/publication/corporate/woolard-review-report.pdf

Financial Conduct Authority. (2022, February 14). FCA drives changes to Buy Now, Pay Later (BNPL) firms’ contract terms. Retrieved from https://www.fca.org.uk/news/statements/fca-drives-changes-buy-now-pay-later-bnpl-firms-contract-terms

Ghosh, D. (2017, September 15). E-commerce catches up to ‘buy now pay later’ credits to reward loyal users. Retrieved from Money Control: E-commerce catches up to ‘buy now pay later’ credits to reward loyal users

Iyer, P. (2021, December 03). Simpl raises $40 million in Series B; Co-founder Clears air on Lawsuit. Money Control. Retrieved from https://www.moneycontrol.com/news/business/startup/simpl-founder-clears-air-on-tussle-with-co-founder-reassures-employees-on-fintechs-roadmap-7788221.html

Johnen, C., Parlasca, M., & Musshoff, O. (2021). Promises and pitgalls of digital credit: Empirical evidence from Kenay. PLoS ONE, 16(7). Retrieved from https://journals.plos.org/plosone/article?id=10.1371/journal.pone.0255215

Jones, R. (2022, January 6). Buy now, pay later customers unaware of debt risks, warns Which? Retrieved from The Guardian: https://www.theguardian.com/money/2022/jan/06/buy-now-pay-later-customers-unaware-of-debt-risks-warns-which

Kaushal, T. J. (2022, January 15). What Happens when you miss your BNPL Payment? Business Today. Retrieved from https://www.businesstoday.in/personal-finance/did-you-know/story/what-happens-when-you-miss-your-bnpl-payment-319222-2022-01-15

Kaushal, T. J., & Adhikari, A. (2022, January 07). The BNPL Mania. Business Today. Retrieved from https://www.businesstoday.in/interactive/longread/the-bnpl-mania-84-07-01-2022

Khatri, B. (2020, December 11). Simpl, LazyPay, and the future of Buy Now Pay Later in India. Retrieved from The Ken: https://the-ken.com/story/simpl-lazypay-and-the-future-of-buy-now-pay-later-in-india/

Kumar, A. (2019, September 1). Credit Score: How do multiple credit inquiries impact your CIBIL score? Retrieved from Financial Express: https://www.financialexpress.com/money/credit-score-how-do-multiple-credit-inquiries-impact-your-cibil-score/1692567/

Kumar, N. (2021, November 10). Using Buy Now, Pay Later scheme for your purchase? This is what will happen if you default on payment. Retrieved from The Economic Times – Wealth.

Kumar, N. (2021, November 29). Watch out for these Costs in Buy Now, Pay Later Schemes. The Economic Times. Retrieved from https://economictimes.indiatimes.com/wealth/borrow/watch-out-for-these-costs-in-buy-now-pay-later-schemes/articleshow/86057163.cms?from=mdr

Live Mint. (2022, January 28). BNPL grew 637% in 2021, recurring payments by 225%, says survey. Retrieved from https://www.livemint.com/money/personal-finance/bnpl-grew-637-in-2021-recurring-payments-by-225-says-survey-11643350720694.html

Makwana, B. (2021, November 19). From Simpl to Paytm Postpaid — These are the Penalties on Late Payments on Buy Now, Pay Later Schemes. Business Insider. Retrieved from https://www.businessinsider.in/personal-finance/news/how-does-buy-now-pay-later-schemes-work-and-what-are-the-penalties-here/articleshow/87788629.cms

Manikandan, A. (2022, February 25). All is not well with India’s BNPL Frenzy. The Morning Context. Retrieved from https://themorningcontext.com/business/all-is-not-well-with-indias-bnpl-frenzy

MicroSave Consulting. (2019, September). Making Digital Credit Truly Responsible: Insights from analysis of digital credit in Kenya. Retrieved from MicroSave Consulting: https://www.microsave.net/wp-content/uploads/2019/09/Digital-Credit-Kenya-Final-report.pdf

Mukherjee, A. (2021, October 7). Buy now, pay later: The craze that’s helping India’s millions of mom-and-pops get access to finance. Retrieved from The Economic Times: https://economictimes.indiatimes.com/industry/services/retail/buy-now-pay-later-the-craze-thats-helping-indias-millions-of-mom-and-pops-get-access-to-finance/articleshow/86827961.cms?from=mdr

Narayanan, V. (2022, February 08). What is Buy Now, Pay Later. Money Control. Retrieved from https://www.thehindubusinessline.com/blexplainer/bl-explainer-buy-now-pay-later/article64970566.ece

Ola. (2021, March 20). Customer Terms and Conditions Postpaid. Retrieved from Ola: https://docs.google.com/viewer?url=https://olamoney.com/images/pdf/Customer_terms_conditions_postpaid.pdf

Pinapala, A. (2021, October 11). Buy now, pay later or party now, worry later: Decoding the latest finance fad. Retrieved from The Economic Times – Industry: https://economictimes.indiatimes.com/industry/banking/finance/buy-now-pay-later-or-party-now-worry-later-decoding-the-latest-finance-fad/articleshow/86931186.cms?from=mdr

Ramanathan, A. (2021, November 22). Buy now, Worry Later: The Indiabulls Dhani Spin on Lending. The Ken. Retrieved from https://the-ken.com/story/buy-now-worry-later-the-indiabulls-dhani-spin-on-lending/

Ramanathan, A., & Kalyanaraman, A. (2022, March 7). Why Ola Postpaid should really be called Ola Loans. Retrieved from The Ken: https://the-ken.com/kaching/why-ola-postpaid-should-really-be-called-ola-loans/

Saxena, A. (2021, July 30). Buy Now Pay Later: The model changing the way credit works in India. Retrieved from Yourstory: https://yourstory.com/2021/07/buy-now-pay-later-changing-credit-loan-landscape-india/amp

Singh, S. (2022, March 17). Does a BNPL platform need your consent to give a loan? . LiveMint. Retrieved from https://www.livemint.com/money/personal-finance/does-a-bnpl-platform-need-your-consent-to-give-a-loan-11647452800864.html

Slice. (2021). General Terms and Conditions. Retrieved from Slice: https://www.sliceit.com/sbmTerms

Wang, P. (2021, February 14). The Hidden Risks of Buy-Now, Pay-Later Plans. Retrieved from Consumer Reports: https://www.consumerreports.org/shopping-retail/hidden-risks-of-buy-now-pay-later-plans-a7495893275/

[1] The authors thank Shreya R (Policy Analyst, the Future of Finance Initiative, Dvara Research) and Hritika Parekh (Intern, the Future of Finance Initiative, Dvara Research) for their valuable contributions in the initial stages of this article.

[2] Lending Service Providers (LSPs) are unregulated entities in the financial sector which partner with REs to provide different services including customer acquisition, underwriting support, pricing support, disbursement, servicing, monitoring, collection, liquidation of specific loan or loan portfolio for compensation from the balance sheet lender. See Reserve Bank of India, Report of the Working Group on Digital Lending including Lending through Online Platforms and Mobile Apps, 2021.

[3] In March 2022, Dvara Research analysed complaints made by customers on Twitter, which surfaced 7 categories of complaints: (1) Difficulties in using the service, (2) Inadequate redress mechanisms, (3) Problems in processing repayments, (4) Wrongful billing, (5) Fraud, (6) Complaints about high charges and fees, and (7) Aggressive debt collection.

The dataset comprised complaints against three prominent BNPL providers – Simpl (3980 tweets), Amazon Pay Later (1558 tweets) and Lazy Pay (9191 tweets) – for the period January 2021 to February 2022. Python was used to collect the tweets, and word clouds and topic analysis were used to identify the issues expressed by BNPL customers. Latent Dirichlet Allocation (LDA) algorithm was used to arrive at the seven categories of customer complaints.

[4] The ten BNPL providers whose terms and conditions we reviewed include Ola Money Postpaid, PayTM Postpaid, Amazon Pay Later, Slice, LazyPay, Simpl, Unicard, Capital Float, EPayLater and Zestmoney.

Cite this Item:

APA

Srikara Prasad, S. S. (2022). ‘Buy Now, Pay Later’: What is it, and how does it affect customer protection? Retrieved from Dvara Research.

MLA

Srikara Prasad, Sarah Stanley. “‘Buy Now, Pay Later’: What is it, and how does it affect customer protection?” 2022. Dvara Research.

Chicago

Srikara Prasad, Sarah Stanley. 2022. “‘Buy Now, Pay Later’: What is it, and how does it affect customer protection?” Dvara Research.