In this study, we explore how borrowers build trust in digital lenders amid the rapid growth of India’s digital credit ecosystem. Read our full paper here.

The presence of digital credit is expanding in India. In 2021, India had nearly 1,100 unique loan apps across various platforms. However, more than half of these were found to be illegal- they operated without proper licensing, promised quick loans without paperwork at questionable terms such as exorbitant interest rates, hidden fees, and used unethical, coercive recovery methods. These practices are in stark contrast with the customer protection guidance offered by the regulator to regulated lenders.

However, at a first pass, it is difficult for customers to differentiate between the two types of lenders—their app designs and user interfaces are often indistinguishable. Assuming borrowers have an inherent preference for more ethical, regulated entities, enabling borrowers to distinguish between the unethical, illegitimate and ethical, regulated lenders is instrumental to effective customer protection in the boundless landscape of digital lending. The ambition of empowering prospective borrowers to identify exploitative digital lenders and defend themselves from those lenders, necessarily, raises two questions: what are the expectations that prospective borrowers have of trustworthy lenders and, how borrowers gauge the trustworthiness of a lender.

An enquiry into the first question allows us to appreciate trust-as-a-process. It surfaces principles and practices that help digital lenders become worthy of customers’ trust. The second question concerns itself with how digital lenders can communicate their trustworthiness to customers. This becomes a pressing issue when the borrower and the lender do not have a prior relationship, and even more important when the borrower is a first-time user of digital credit. Data suggests that about 140 million Indians became first-time borrowers between 2019 and 2022. A significant portion of these new credit customers are low-income households earning under Rs 2.8 lakh per year, with digital lenders playing a key role in serving them. This study focuses on how lenders can become worthy of borrowers’ trust. In the order of questions, this must be wrestled with first because enabling lenders to communicate trustworthiness without them actually becoming trustworthy would be a bigger disservice to the customer protection agenda.

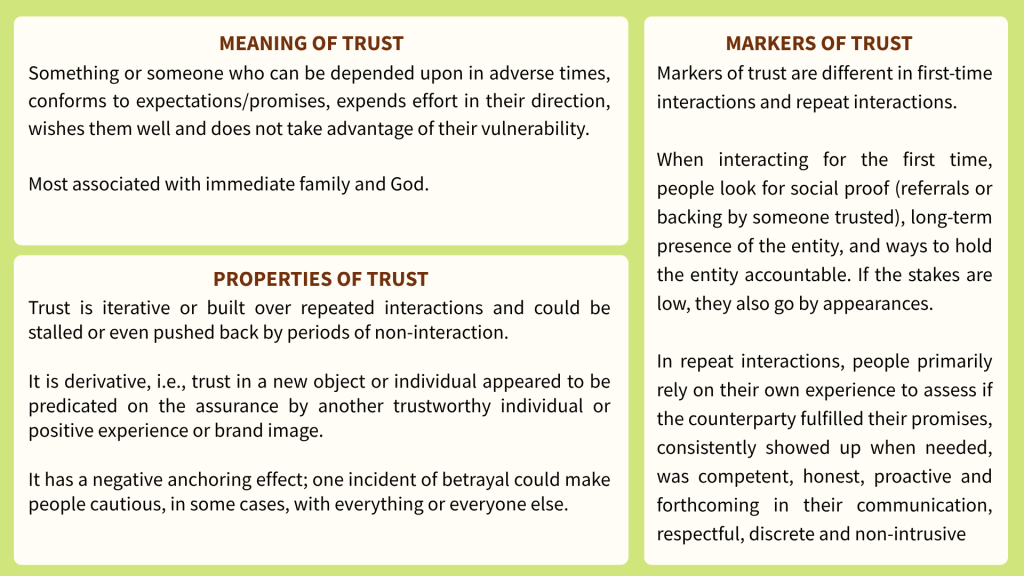

The study seeks to understand how customers trust and contract with a digital lender. Uncovering what people mean by trust by directly asking them about it can be difficult, partly because the word trust has a dual nature- it is both a noun and a verb. Owing to this dual nature, it is difficult to define trust without implicating trust itself. Instead, we attempt to study trust in terms of the proximate grounds that people rely on to trust someone or something. To explore the proximate grounds customers rely on to trust digital lenders, we commenced a mixed-methods study of DFS users in early 2024. The study is supported by qualitative interviews spanning a range of topics from what trust meant in personal relations and financial transactions to the obligations that come with being considered trustworthy. This is complemented by an experiment where respondents assess the user interfaces of digital lending apps for trustworthiness. Based on our discussions with DFS users, we develop a theory to explain the making of trust in digital lending.