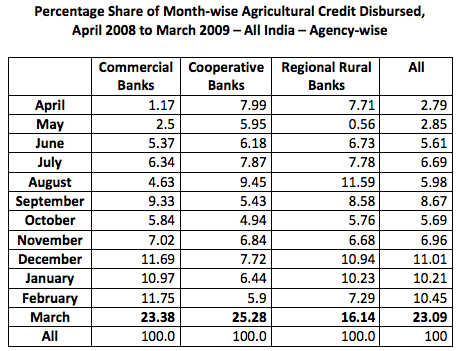

The Task Force on Credit Related Issues of Farmers, chaired by Umesh Chandra Sarangi, in its report submitted to the Ministry of Agriculture, Government of India, in 2010, observes that while month-wise credit disbursement patterns should have been in line with ground level requirements of kharif (June, July, September) and rabi (December, January), one-fourth of the disbursements instead happen in March, a month that is not critical to agriculture production.

Below table and the interactive chart throws light on this:

Many of the reasons cited by the report for this phenomenon are likely to be direct consequences of having year-end priority sector lending targets for banks.

9 Responses

Thanks for this – most illuminating as always. Also, mad props for not using an Excel chart.

Would love to see you guys frame the topic of public sector lending in the perspective of agricultural credit in election and non-election years, as an update of Shawn Cole’s famous paper: http://sites.google.com/site/sacole/elect-07-04-02.pdf

Sir,

This may also lead us to think on the fundamental skewed year-ending fixed in March. It should be fixed to coincide with the agricultural cycle, which is also the natural phenomenon or ‘rutu-chakra’.

Does it require a study to draw this conclusion? Last fortnight and more particularly last week of month of March every year are the periods for banks when both loans and deposits are shown at their peak level. In the first week and first fortnight of April every year, the steep fall in deposit figures and a moderate fall in loans and advances figures can also be noticed. It is not just the priority sector lending alone is the cause for this shoot up in loan figures. It is window dressing exercise resorted to by all banks (forcing the clients to draw the full amount of sanctioned limits and park the funds in short term deposits is one example). With SHG loans brought under Cash Credit type of operations, you may find this phenomenon in coming years. Perhaps, IFMR may mount a study to look at this in 2014-15 (April 2014) as this year is the first year after shifting to CC pattern of lending.

Thanks Sir. In the same vein, lending through

the Kisan Credit Card (which also qualifies under PSL), also originally

intended as a cash-credit facility, would be worthy of further study. However, the

cash-credit limit, being considered to be too small for its use as a credit

card, has been known to be usually fully used up by the KCC holder to avail a

one-shot loan. It will be interesting to see how the same would work under the

SHG model.

As Mr Santhanam has pointed out, its the usual rush to meet year-end targets. Lest we beat up the banks. this also exactly what corporate businesses do! The way around this is for govt to review the priority sector agriculture portfolio on a time scale related to agri. This will ensure faster disbursal of eligible applicants when they need their money. Its quite likely they incur costs of borrowings – either through actual borrowing or prices that capture the delay.

Thanks Sir. The post was intended to indicate the burden that unwittingly gets imposed on farmers due to the placement of PSL targets at the end of the FY (perhaps done so as a matter of convenience from the point of view of target-achievement and monitoring). From the point of view of a farmer, a loan taken in March for cultivation, which cannot be deployed until a few months later when the next agriculture season commences – would impose unwarranted servicing costs on the farmer, besides the use of the loan amount for other purposes.

It is very clear that meeting the targets has not spared the field of agriculture too.By the way an analysis with respect to the purpose of loans disbursed on monthly basis may be an eye opener.

Thanks Ma’am. On the same lines, an analysis of which sub-categories under PSL get what proportion of credit during which months – would help tremendously to refine the argument.

Thats really a great statistics – Looking for More banking information.