The Prime Minister’s Garib Kalyan Yojana announced on 26th March 2020 sets out some important and very welcome steps in addressing the COVID-19 crisis. These include cash transfers to the most vulnerable sections of society and an increase in MNREGA wages. Crucially, the Finance Minister announced an insurance cover for frontline health workers putting themselves at risk through the COVID-19 lockdown. The Ministry of Finance has stated that all “safai karamcharis, ward-boys, nurses, ASHA workers, paramedics, technicians, doctors and specialists and other health workers” who “meet with some accident” while treating COVID-19 patients, will be compensated with a sum of Rs. 50 lakhs.

Providing life and accident insurance cover to frontline workers is an important step in this crisis. However, the policy announcements do not encompass all the workers who may be at risk during this time. The central government has clarified that essential service, including PDS and other grocery shops, pharmacies, transport of essential goods, banking staff and business correspondents, will continue to remain functional during the period of lockdown. Many of these workers, who go from door to door, or come into contact with large numbers of people, are also at a high risk of contracting COVID-19. Many of these workers – those who operate small pharmacies, for instance, or who work for food delivery aggregators – work outside formal government structures. The insurance scheme proposed must, therefore, be extended to all classes of workers required to provide services during the period of lockdown.

Health Insurance for those affected by COVID-19

A bigger concern, however, was the lack of clarity on health insurance for in-patient treatment of those affected by COVID-19. The governments of Bihar, Maharashtra and Odisha have announced that free treatment will be provided to patients suffering from COVID-19 in government hospitals. However, it must be stressed that India has limited capacity to address this crisis – with only 2.3 critical care beds per 100,000 inhabitants as against 34.7 in the United States. Additionally, there are only about 40,000 ventilators in the entire country. Many of these are in private hospitals. While there is a need to expand health care capacity in the long term, in the immediate term, it is vital that patients have access to all available facilities for treatment. This would include the ability to care for COVID-19 patients at home if they do not require hospitalisation.

However, the recently announced relief package does not address insurance cover for expenses incurred while treating those infected with COVID-19. This is problematic, as many Indians do not have access to any alternate cover. A recent IRDAI notification requires all insurance companies to cover and “expeditiously handle” all claims made for treating COVID-19, including those made under the Central Government’s flagship Ayushman Bharat Yojana. However, while Ayushman Bharat is intended to cover over 10.74 crore deprived households, data from the PMJAY website shows that only 25% of beneficiaries have received their Ayushman Bharat e-cards.[1] Meanwhile, only a small portion of the workforce (i.e., the organised sector) has access to insurance under the ESIC scheme. On the whole, health insurance penetration in India is poor – in one survey by CMIE, only 22% of respondents stated that they had access to health insurance.[2]

In the short term, we propose that the criteria for inclusion in AB PM-JAY be relaxed, and all households without alternate insurance cover be permitted to self-enrol under the scheme for COVID-19 treatment. The scheme must expressly provide for cashless treatment – as Dvara Research noted in a recent policy brief, many households may lose their source of income during the lockdown. A reimbursement model of health insurance would, therefore, not provide adequate coverage. In states which have opted out from the ABY scheme – Delhi, Telangana, Odisha and West Bengal – we suggest that the respective state schemes be expanded to provide insurance cover to all households in need of treatment at this time. [3]

Additionally, it is important to ensure that treatment is available in the maximum number of facilities, in other words, to ensure that hospitals can be empanelled at short notice. We suggest that all designated hospitals for COVID-19 treatment – with appropriate testing, treatment and isolation facilities – be empanelled on an emergency basis, provided that they meet the accreditation criteria of the National Board.

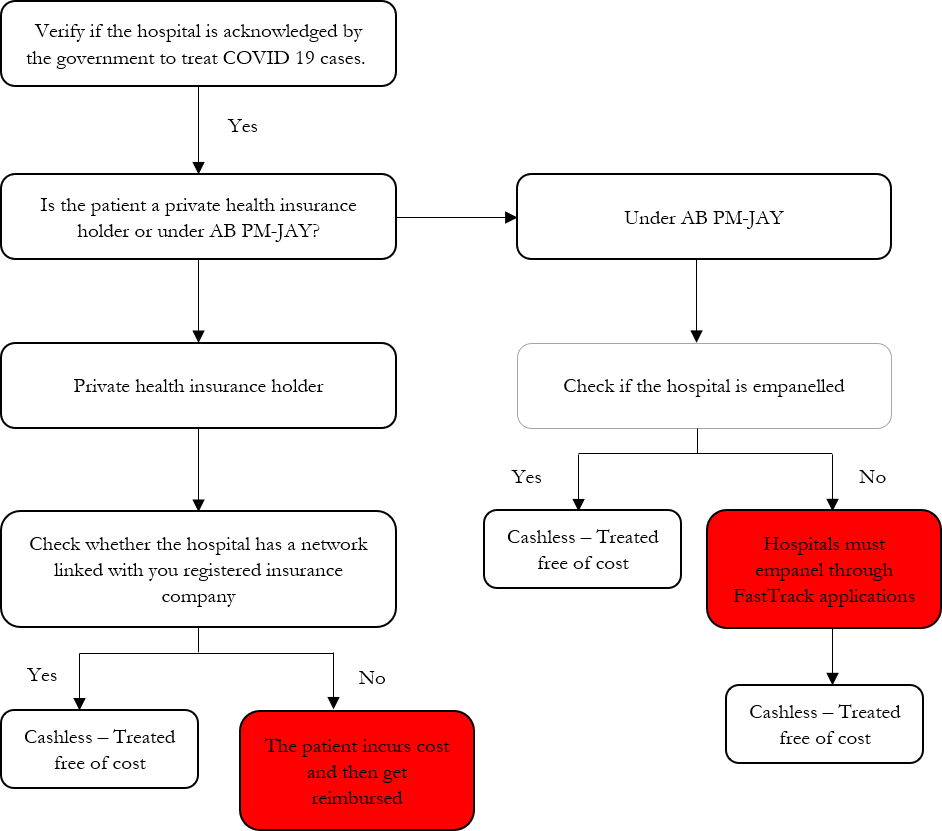

The flowchart below sets out the different possibilities for treatment at a hospital during the lockdown:

The 21-day lockdown and the recent relief package are important steps in preventing the spread of COVID-19. However, it is equally important to ensure that those who are exposed to the illness are protected. Expanding both the accident insurance cover for frontline workers as well as the availability of cashless treatment through publicly funded health insurance programmes is vital at this time.

__

[1] Calculated by authors based on data from https://pmjay.gov.in/

[2] Calculated from the CMIE-CPHS survey for the wave Sept-Dec 2019.

[3] Odisha has announced that Covid-19 patients will be treated in two new facilities designated for this purpose.