Internal migration is a prominent feature of a developing economy. The high rural-urban wage gap in a country like India pushes the households to send a migrant away in search of work. Migration has two strands: permanent and temporary. In permanent migration, the entire household leaves the place of origin and moves to the workplace. In temporary migration, the household sends the earning member of the household away to the workplace (typically male members). Temporary migration has been increasing in India over the years. Some estimates show that 20 per cent of the rural households have at least one temporary migrant with temporary migration representing more than 50 per cent of the total income (Morten, 2019). Migration increases nominal income for the entire household. However, it also increases the household risk as the earning member of the household is always on the move. The recent COVID-19 crisis has highlighted the scale of internal migration in India and related risk.

The usual components of household risks in the rural economy include health shock, loss of asset, loss of livelihood, village level or macroeconomic shocks and other idiosyncratic shocks. Due to credit and insurance market imperfections, these expenses are borne from the household portfolio or informal networks (Duflo and Banerjee, 2011). Apart from those mentioned above, a migrant faces numerous other risks. First, temporary migrant face travel risks, especially for frequent travellers. Commuter and short duration migrants (who spend less than a month at the workplace) frequently travel between the place of origin and workplace destination. The mode of transport, which is a bike or crowded public transport, increases the chance of accidents. Second, most of the migrants work in the informal sector, such as construction activity and restaurants. These sectors do not provide proper social protection and job security to the workers. This is a major risk for the migrant worker at the work destination. Third, inter-state migrants have to bear a higher risk due to the non-portability of state benefits/protection. They also have reduced social capital due to no/smaller social network at the workplace. It makes them dependent on the contractor or the employer in case of emergencies. This reduced social capital with long period away from the family affects the household’s well-being.

In summary, the risks or shocks specific to temporary migrants are:

-

Risk involved in commuting long distances

-

Low quality of work at destination, some involving serious long-term health hazards

-

Informality of work with the absence of an enforceable contract and job security

-

Lack of necessary and adequate social security protective measures

- Challenge of non-portability of state-specific benefits faced by inter-state migrants

-

Erosion or complete loss of social capital/social network due to frequent relocation from source to destination

Households rely on different sources of finance to overcome negative shocks such as formal credit, insurance, informal risk-sharing network and household asset portfolio. Insurance and formal credit markets can only cover the partial risk. The rural households still have to rely on informal networks and household asset holding, especially during an emergency. A diversified household portfolio with liquid, tangible assets, along with regular savings, can provide resilience to overcome shocks. But it is observed that household portfolio in developing economies is skewed towards tangible assets such as real estate and gold (Badarinza, Balasubramaniam, and Ramadorai, 2019). Liquid assets have a low share in their portfolio.

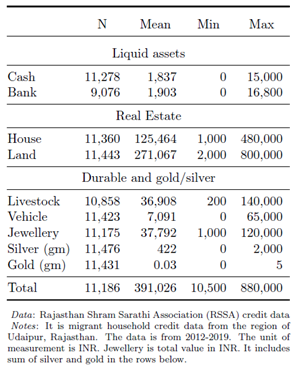

In recent research conducted as a Fellow, we use administrative data from Rajasthan Shram Sarathi Association (RSSA).[1] It provides credit to migrant households exclusively. Table 1 shows the asset allocation in a migrant household using RSSA data. It is clear from the table that the migrant household allocation is no different from the average Indian household. It has a significant share of real estate and durables in the portfolio. Interestingly, there is heavy investment in silver and livestock in the region of Udaipur. The share of a liquid asset is approximately 2000 INR in cash and deposit each. The liquid asset holding is not sufficient to overcome the unexpected negative shock.

Anecdotal evidence of Javana (name changed) a resident of Patiya-Gogunda, a hamlet near Udaipur, demonstrates the vagaries of a migrant household. Javana has a small four-member family comprising of his parents and wife. The household asset portfolio resembles an average rural household structure with real estate, silver, livestock, and cattle covering the majority of the portfolio value. Javana is a migrant worker. In 2018- 19, he worked in Udaipur along with his wife, Homli Bai. They both travelled daily 50 km to the workplace on their bike. Travelling daily on the bike reduced the living cost at the workplace, however, it also increased the risk of an accident.

Once while returning to the village at night, Javana and his wife met with an accident on the national highway. Fortunately, there were minor injuries. But they both could not work for a month that reduced their income stream. Javana was not able to pay bike instalment on time and had to borrow from other sources to pay the instalments. The fear of accident made the household to change their work choices. Homli bai dropped out of the labour force. Despite having higher returns, the family discouraged Javana from travelling to Udaipur daily. He found a job in the neighbouring district of Rajasmand through his family networks. However, this meant he would be staying away from the family and visiting the village once a month. He moved from being a commuter migrant to short duration migrant. Apart from the accident, the household also faced the death of cattle due to a disease which leads to cattle deaths in the entire village. This reduced the cushion in the asset portfolio. The likelihood of multiple shocks puts the migrant household at a higher risk frontier.

Table 1: Asset holding structure in migrant households

Temporary migration, despite being a risky venture, provides an option to earn higher income for the rural poor (Bryan, Chowdhury, and Mobarak, 2014). However, these gains do not provide sufficient support to absorb unexpected negative shocks in a migrant household. Thus, there is a need to build diversified and more resilient portfolios for rural households to overcome risk. Further, reducing the credit market imperfections at the place of origin, particularly including insurance for human capital and assets may provide larger gains.

All views are those of the author and do not necessarily reflect those of Dvara Research.

References

Badarinza, Cristian, Vimal Balasubramaniam, and Tarun Ramadorai (2019). “The household finance landscape in emerging economies”. In: Annual Review of Financial Economics 11, pp. 109–129.

Bryan, Gharad, Shyamal Chowdhury, and Ahmed Mushfiq Mobarak (2014). “Underinvestment in a profitable technology: The case of seasonal migration in Bangladesh”. In: Econometrica 82.5, pp. 1671–1748.

Duflo, Esther and Abhijit Banerjee (2011). Poor economics. Public Affairs.

Morten, Melanie (2019). “Temporary migration and endogenous risk sharing in village India”. In: Journal of Political Economy 127.1, pp. 1–46.

[1] The Rajasthan Shram Sarathi Association and the Household Finance Research Initiative at Dvara Research offered the Fellowship for conducting research on themes in household finance of migrant households in India. The research using RSSA data is part of the research fellowship.