This blog is the second in our two-part series on nano-enterprises, building on the discussion introduced in Part 1.

Nano entrepreneurs constitute the majority of last-mile borrowers in India, yet they face significant constraints in accessing credit. Although India has approximately 7.7 crore[1] nano-enterprises, only a small fraction currently has access to formal credit channels. Formal financial institutions often exclude those who are New to Credit (NTC) or have thin credit files, thereby constraining the growth potential of enterprises that are seeking to expand. This exclusion is largely because such enterprises are unable to demonstrate creditworthiness due to the absence of a digital trail, formal cash-flow records, or lack of suitable collateral.

However, nano-enterprises in India display considerable heterogeneity in their need for credit, with enterprises ranging from subsistence level operations to emerging growth-oriented ones. For instance, Own Account Enterprises[2] (OAEs) which are typically solo entrepreneurial ventures have relatively adequate access to credit, with over-lending emerging as a key concern[3]. In contrast, Hired Worker Enterprises[4] (HWEs), which employ up to five workers on a regular basis, are severely underfunded and receive only a fraction of the credit they demand. Investment needs also vary widely, ranging from as low as ₹50,000 to as high as ₹25 lakh. Furthermore, within HWEs, there is also an aspirational segment employing more than 10 workers and requiring investments exceeding ₹1 crore. These enterprises also have distinct financing needs which include micro-equity for fixed capital investments and cash-flow based loans for working capital[5].

Given such a heterogeneity, the central challenge is not merely expanding credit supply, but identifying which enterprises require credit, what type of credit is most suitable[6], for what purpose, and at what scale. Without such differentiation, credit interventions risk either over-indebting subsistence enterprises or under-serving growth-oriented enterprises.

Why Heuristics Matter for Classifying Nano-enterprises[7]

Heuristics are useful analytical devices precisely because they simplify complex and heterogeneous economic realities without claiming to exhaustively describe them. Heuristics also help to foreground “institutional variety” and “functional differences” that are often obscured by standard microeconomic classifications based solely on firm size or sector[8]. In the context of Indian nano-enterprises, heuristics enable classification along dimensions such as growth orientation, capital investment, turnover, labour employed and financing needs, thereby capturing meaningful differences. Such heuristic classification supports more context-sensitive policy design by recognising that these enterprises operate under distinct constraints, incentives, and institutional arrangements.

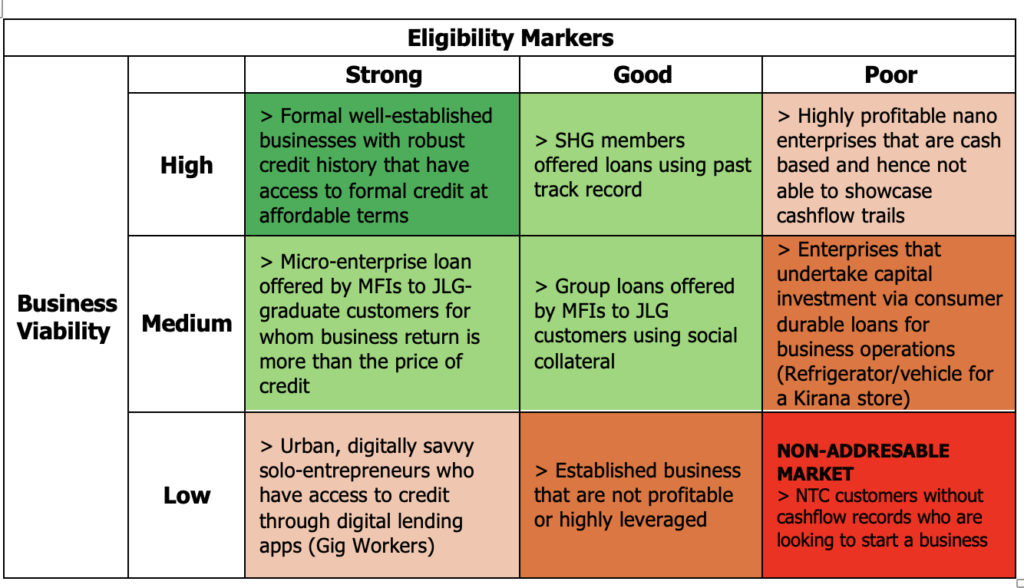

From a lender’s perspective, identifying relevant enterprises for formal credit can happen along two dimensions: Business Viability and Eligibility Marker. Business viability reflects internal firm-level dynamics that shape repayment capacity, whereas eligibility captures lender-facing characteristics that determine whether an enterprise can demonstrate their creditworthiness in the eyes of the lender While the two dimensions, are not entirely exclusive and influence each other, this heuristic treats them as distinct categories.

In Table 1, we envision different typologies of nano-entrepreneurs across the two axes – one on their inherent business viability and the other on their ability to prove eligibility for formal loans. Those in the dark green zone are ideal customer cohorts with inherently high business viability and strong eligibility markers for whom the credit market already works well. Those in the pale green zone are the transition cohorts, representing medium levels of business viability and fairly good eligibility markers. The dark red zone characterized by low levels of viability and very poor eligibility markers represents the non-addressable market. It is the orange zone, where any intervention in credit provisioning could work to improve outcomes for nano-entrepreneurs. Here, the dark orange zone (with either medium viability and poor eligibility markers or low viability with good eligibility markers) represents cohorts for whom alternative arrangements, though sometimes informal, seem to be working. For credit to be formalized for this cohort, they need other non-credit interventions that improve the nature of their enterprise.

The pale orange zone is characterized by two contrasting profiles: enterprises with low business viability but strong eligibility markers, and those with high viability but weak eligibility markers. This segment presents a strong case for targeted credit-led intervention, as improving performance along the dimension they are weaker can shift these enterprises into a more viable credit zone. This can simultaneously enhance credit accessibility and affordability for enterprises while strengthening lender sustainability. Therefore, by identifying the right cohorts for an intervention, we can solve not just accessibility and affordability for nano entrepreneurs but also for cost-effectiveness and sustainability of the lender.

Table 1: Typologies of different nano-enterprise profiles with Illustrative Examples

Population Distribution Across Heuristic Cohorts

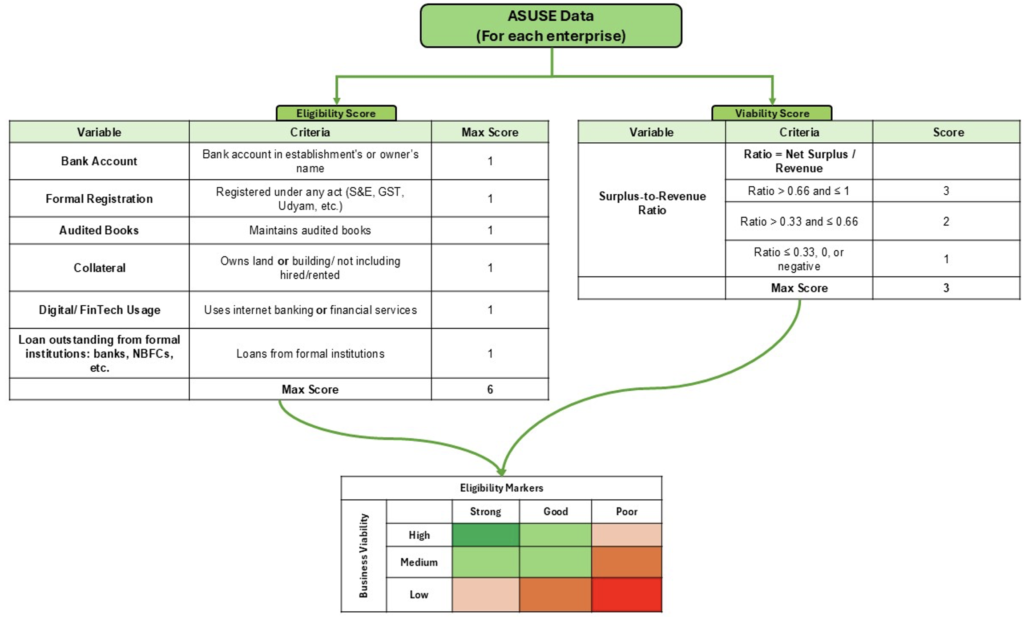

The heuristic-based classification of nano-enterprises can be applied to unit-level data from ASUSE 2023–24 to generate population-level estimates[9]. As mentioned earlier, this approach is motivated by the heterogeneity within the nano-enterprise segment, which makes classifications based solely on firm size (turnover or investment) or employment thresholds very limited.

The eligibility score is constructed using six binary indicators observable in ASUSE: ownership of a bank account, formal registration, maintenance of audited accounts, ownership of collateral, use of digital or fintech services, and presence of outstanding loans from formal financial institutions. Each indicator is assigned equal weight, yielding a score bounded between zero and six. Higher values indicate greater ease with regards to formal lending eligibility criteria

The viability score, derived from the surplus-to-revenue ratio, is calculated as net surplus divided by total revenue. Here, enterprises are assigned discrete scores based on threshold values of this ratio, with maximum viability score of three. Lower or negative surplus indicating greater financial vulnerability (lower score) and hence lower business viability.

The eligibility and viability scores are jointly used to place an enterprise onto a two-dimensional plane, as depicted in Figure 1. Further, survey weights from ASUSE are applied to compute nationally representative estimates of enterprises within each cell of the grid. These cells are interpreted as heuristic cohorts reflecting distinct combinations of eligibility and business viability markers.

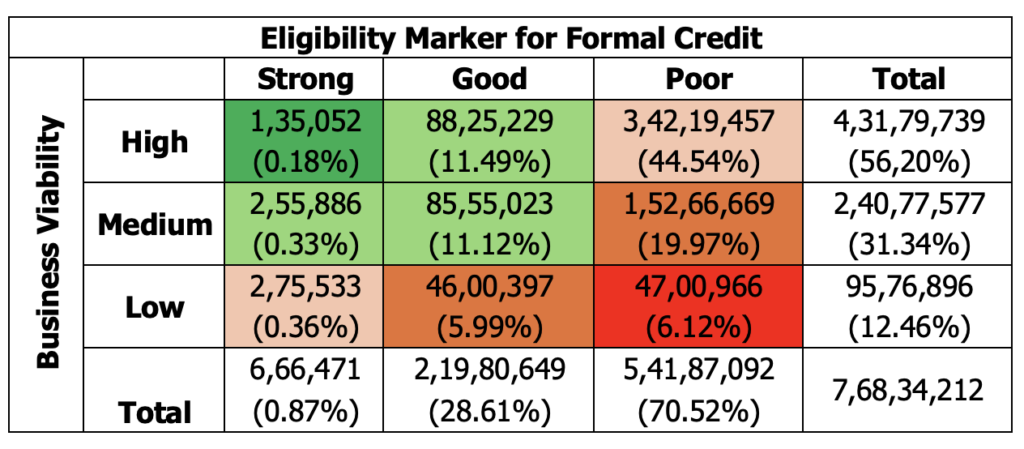

Table 2 reports the resulting population-level distribution, demonstrating significant heterogeneity in both eligibility and viability within the nano-enterprise segment. Of those that could serve as potential borrowers, particular attention needs to be given to those who are characterised by poor eligibility but have inherently high business viability (top-right segment of table). These come to around 3.42 Cr enterprises or 44.5% of the entire firms in the nano-enterprise universe. While not all of these enterprises may desire or require formal credit, this segment potentially represents the group for whom access to formal finance might be a binding constraint. Despite being in relatively sound financial condition, many lack one or more eligibility markers required to be considered creditworthy by formal financial institutions. This makes them a key target group for interventions aimed at improving credit access where appropriate.

Figure 1: Illustration of how eligibility and viability scores are jointly used

Table 2: Population level estimates from ASUSE 2023-24

Common Characteristics of Nano-Enterprises with Low Eligibility Score and High Business Viability Score

This section provides some key characteristics of our target cohort highlighting their underlying profiles.

As shown in Table 3, bank account access among nano enterprises is relatively widespread at 62.1%, covering about 2.1 Cr enterprises. In contrast, formal registration remains limited to just 9.0% (around 0.3 Cr), while bookkeeping practices are almost non-existent. Land or building ownership is comparatively high at 73.4%, accounting for nearly 2.5 Cr enterprises. The adoption of digital finance is very low at only 3.0% (approximately 0.1 Cr), and access to formal loans is negligible at 0.2%, representing roughly 81,000 odd nano enterprises. Hence, this segment is characterized by limited engagement with formal finance, with 38% lacking bank accounts and 96% not using any form of digital payments.

| Variable | Yes (Count, %) | No (Count, %) | Missing (Count, %) | Total |

| Has a bank account | 2,12,43,195

(62.08%) |

1,29,76,262 (37.92%) | 0 (0.00%) | 3,42,19,457 |

| Has formal registration | 30,94,199

(9.04%) |

3,11,25,258 (90.96%) | 0 (0.00%) | |

| Maintains audited books | 42

(0.00%) |

3,42,19,415 (100.00%) | 0 (0.00%) | |

| Owns land or building | 2,50,99,740

(73.35%) |

41,18,484

(12.04%) |

50,01,233

(14.62%) |

|

| Uses digital finance | 10,11,987

(2.96%) |

13,62,476

(3.98%) |

3,18,44,994

(93.06%) |

|

| Has formal loan(s) outstanding | 81,120

(0.24%) |

9,64,871

(2.82%) |

3,31,73,466

(96.94%) |

Table 3: Summary of selected nano-enterprise cohort characteristics

The aforementioned nano-enterprise cohort distribution is heavily skewed toward smaller units with 90% of firms having turn-over less than ₹10 Lakhs (Table 5). They are also largely rural (56.8% or 1.9 Cr), operate within household premises (55.0% or 1.8Cr) and pre-dominantly employ less than 5 workers (Table 4, 5 & 6). Majority (90%) of firms largely engage in the following sectors Trade (Wholesale & Retail), Manufacturing, Real Estate & Rental, Personal & Household Service and Transport, Warehousing & Logistics (Table 9). Notably, over 64% of the cohort are concentrated in trade and manufacturing, underscoring the dominance of low-margin, working-capital-intensive activities.

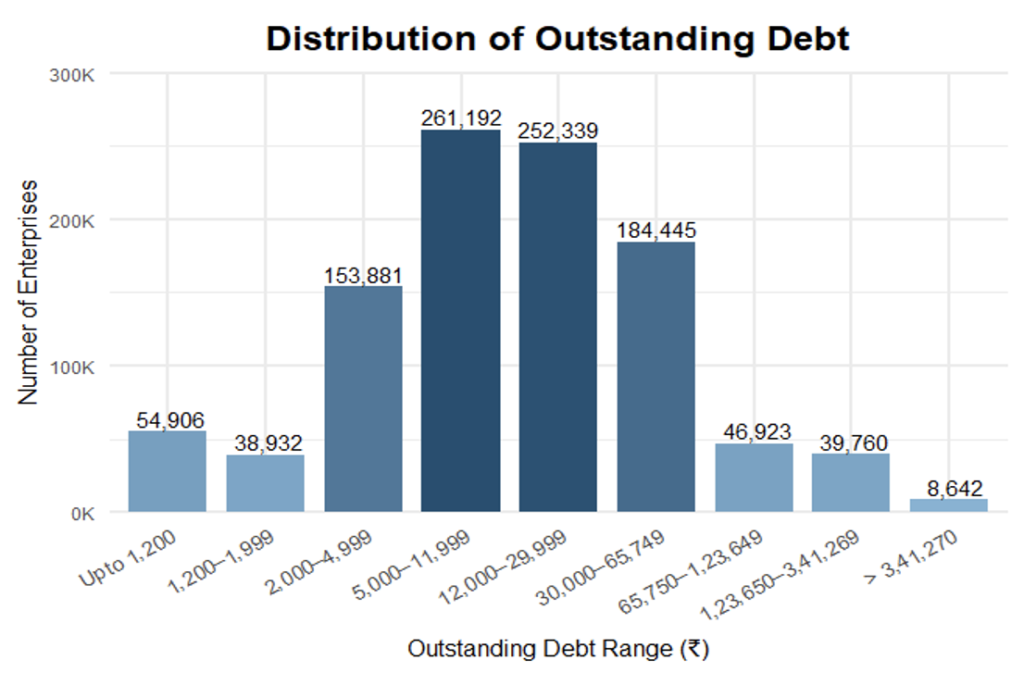

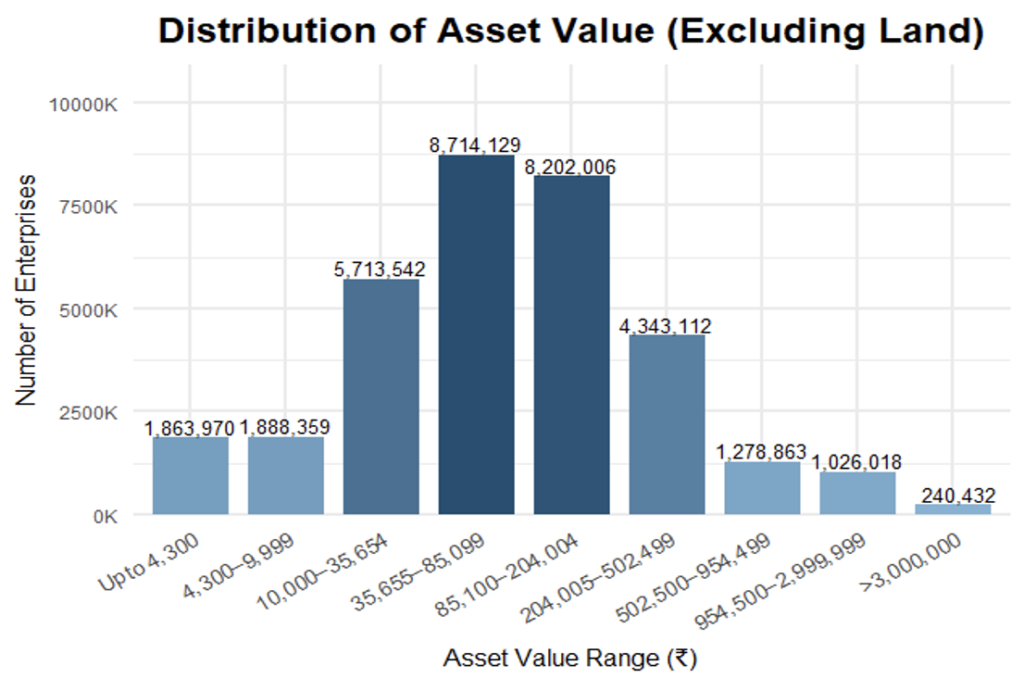

Figures 2 and 3 indicate low leverage and modest asset bases of these enterprises. Debt remains minimal as only 3% of the firms have any outstanding debt with majority (42%) owing less than ₹10,000. Excluding land[10], the asset size of these firms is also severely constrained with 11% holding assets worth less than ₹10,000 and 92% of the enterprises having less than ₹5,00,000 in assets. For enterprises seeking to expand, such limited balance-sheet depth may constrain their ability to access formal credit or undertake larger investments.

| Turnover | Enterprises | Percent |

| Below 10 lakh | 3,10,87,238 | 90.95 |

| 10–25 lakh | 26,21,439 | 7.67 |

| 25–50 lakh | 3,84,204 | 1.12 |

| 50 lakh–1 Cr | 87,025 | 0.25 |

| Total | 3,41,79,906 | 100 |

Table 4: Distribution of selected nano-enterprise cohort by Turnover

|

Geography |

||

| Type | Enterprises | Percent |

| Rural | 1,94,24,676 | 56.83 |

| Urban | 1,47,55,230 | 43.17 |

| Total | 3,41,79,906 | 100 |

Table 5: Distribution of selected nano-enterprise cohort by Geography

|

Location of Establishment |

||

|

Description |

Enterprises | Percent |

| Within household premises | 1,88,07,704 | 55.03 |

| Outside (with fixed premises and with permanent structure) | 74,97,096 | 21.93 |

| Outside (with fixed premises and with temporary structure / kiosk / stall) | 6,90,041 | 2.02 |

| Outside (with fixed premises but without any structure) | 7,03,179 | 2.06 |

| Outside (mobile market) | 11,66,284 | 3.41 |

| Outside (without fixed premises: street vendors, etc.) | 53,15,603 | 15.55 |

| Total | 3,41,79,906 | 100 |

Table 6: Distribution of selected nano-enterprise cohort by Type of Establishment

| Total Workers | ||

| Total Workers | Enterprises | Percent |

| 1 | 2,78,98,204 | 82.32 |

| 2 | 52,08,806 | 15.37 |

| 3 | 6,63,728 | 1.96 |

| 4 | 84,019 | 0.25 |

| 5 and more | 35,176 | 0.11 |

| Total | 3,38,89,931 | 100 |

Table 7: Distribution of selected nano-enterprise cohort by employed workers

|

Group |

NIC 2-digit codes included | Enterprises | Percent |

| Trade (Wholesale & Retail) | 45, 46, 47 | 1,13,09,269 | 33.09 |

| Manufacturing (All) | 10–33 | 1,06,16,345 | 31.06 |

| Real Estate & Rental Services | 68, 77 | 40,77,711 | 11.93 |

| Personal & Household Services | 55, 56, 93, 95, 96 | 33,32,295 | 9.75 |

| Transport, Warehousing & Logistics | 49, 50, 52 | 14,22,520 |

4.16 |

Table 8: Distribution of selected nano-enterprise cohort by Activity

Figure 2: Distribution of selected nano-enterprise cohort by outstanding debt

Figure 2: Distribution of selected nano-enterprise cohort by outstanding debt

Note: The buckets divide enterprises into percentile groups based on their outstanding debt, ranging from the lowest 5% of enterprises to the top 1% with the highest debt levels.

Figure 3: Distribution of selected nano-enterprise cohort by assets (excluding land)

Note: The buckets divide enterprises into percentile groups based on their assets, ranging from the lowest 5% of enterprises to the top 1% with the highest asset levels.

Conclusion and Way Forward

Nano-enterprises in India constitute a highly diverse and non-homogeneous segment, exhibiting wide variation in scale, sectoral distribution, formalisation, financial viability, and credit characteristics. We propose a heuristic-based framework as one way of organising this heterogeneity, using observable indicators of credit eligibility and business viability to showcase analytically meaningful cohorts for identifying enterprises that could benefit from tailored interventions. A deeper understanding of these heterogeneous segments enables the design of targeted incentives for nano-enterprises. For those enterprises with high business viability yet poor eligibility markers, interventions can focus on facilitating Udyam registration to integrate them into the formal ecosystem and UPI enablement to digitise transactions and generate verifiable cash flow records. Creating digital transaction trails, coupled with business registration via Udyam and basic compliance, allows lenders to better assess business viability of these enterprises. In addition, blended finance (BF) instruments such as credit guarantees, concessional financing, or outcome-based financing can help de-risk lending to these enterprises and catalyse greater access to formal finance. While the proposed heuristic offers a useful lens, it is not exhaustive and alternative classifications may be equally valid depending on explicit policy objectives and data sources used. Importantly, policy making aimed at unlocking credit for nano-enterprises must move beyond uniform interventions and explicitly account for this underlying diversity to design more effective and context-sensitive solutions.

Part 1 of the series can be accessed here.

Footnotes:

[1] Annual Survey of Unincorporated Sector Enterprises (ASUSE) 2023-24 Microdata

[2] OAE (Own Account Enterprises): Enterprises that operate without hiring any regular paid workers and are typically run by self-employed individuals or family members.

[3] Mahajan, V., & Bhargava, P. (2025). SME Financing—How to Bridge the Persistent Demand Supply Gap? https://doi.org/10.2139/ssrn.5141173

[4] HWE (Hired Worker Enterprises): Enterprises that employ at least one regular paid worker in addition to the owner

[5] Bhargava, P., & Mahajan, V. (2025). Architecting India’s Credit DPI For High-Growth MSMEs. https://doi.org/10.2139/ssrn.5284150

[6] Credit is considered suitable when it is accessible, affordable, and relevant to the context and needs of its target segment

[7] The heuristic laid out in this article was developed by Priyadarshini Ganesan and the author gratefully acknowledges her support in developing the idea behind this blog.

[8] Srinivas, S. (2021). Heuristics and the microeconomics of innovation and development. Innovation and Development, 11(2–3), 281–302. https://doi.org/10.1080/2157930X.2021.1986894

[9] ASUSE 2023–24 provides nationally representative, unit-level data on unincorporated non-agricultural enterprises in India

[10] Land is excluded as it is typically illiquid, not directly tied to business operations, and may reflect household wealth rather than the productive capacity of the enterprise.

One Response

Very interesting blog, both this and the first part in the series. Forced me to think about how the more qualitative aspects of running a business tend to be overlooked in financial reports, and circumstantially having effect on overall perception and decisions made about these businesses.