In April, the Future of Finance Initiative (FFI) hosted a series of closed door workshops with a small set of digital financial service providers focusing on payments, credit and investments. The primary goal of the workshops was to map the “transaction journeys” of individuals using digital financial services in India and identify points of weakness from a supply side perspective. This helped us get a clearer understanding of the emerging customer level vulnerabilities in the Indian digital financial landscape. This blog summarises key insights from the first workshop that we hosted on digital payments. The discussions were held under the Chatham House Rule, so this post is limited to overall themes without attributing comments to participants. We thank the participants for their frank and open views presented at the discussions.

The payments ecosystem in India has undergone rapid evolution in the recent past. Post demonetisation, the big push from Government to scale up digital payments has been front-and-centre on the policy and industry agenda. Given all of this, we wanted to understand:

- How are providers providing solutions relevant to new market segments?

- Where are the risks and vulnerabilities across the chain of the players and processes associated with making a digital payment?

We posed some of these questions to the carefully curated set of participants of the digital payments workshop. They reflected players across the payments ecosystem in India including wallets, payment system operators, payment gateways, card payment processors and software developers.

New customer segments need new products tailored to their needs

The workshop kicked off with a discussion on broad trends and considerations emerging for those working in the payments industry in India. A key observation was that new segments of customers are being brought into the digital payments ecosystem who are different in their capacity to absorb any losses, compared to existing customers. This opens up new opportunities and responsibilities for providers, including on product design and innovation.

The workshop kicked off with a discussion on broad trends and considerations emerging for those working in the payments industry in India. A key observation was that new segments of customers are being brought into the digital payments ecosystem who are different in their capacity to absorb any losses, compared to existing customers. This opens up new opportunities and responsibilities for providers, including on product design and innovation.

Specifically, financial services tailored for low income consumers, have not evolved in the Indian financial market — unlike other sectors such as telecommunications (where for e.g. different levels and durations for phone recharges are available). As an illustration, most credit cards are set up for 45 days cycles as they are aimed to cater to “salaried’ employees who earn once a month. However, there are no cards with 20 days cycles for people earning twice a month or at more frequent intervals (such as those in part-time work or the informal sector). In the future, such a segment could be served by small finance banks and payment banks, potentially in partnership. Some participants felt that this approach to banking could be a more effective for fostering financial inclusion than recent government schemes which scale-up inflexible products (such as no-frills bank accounts).

Services providers in the chain of payments

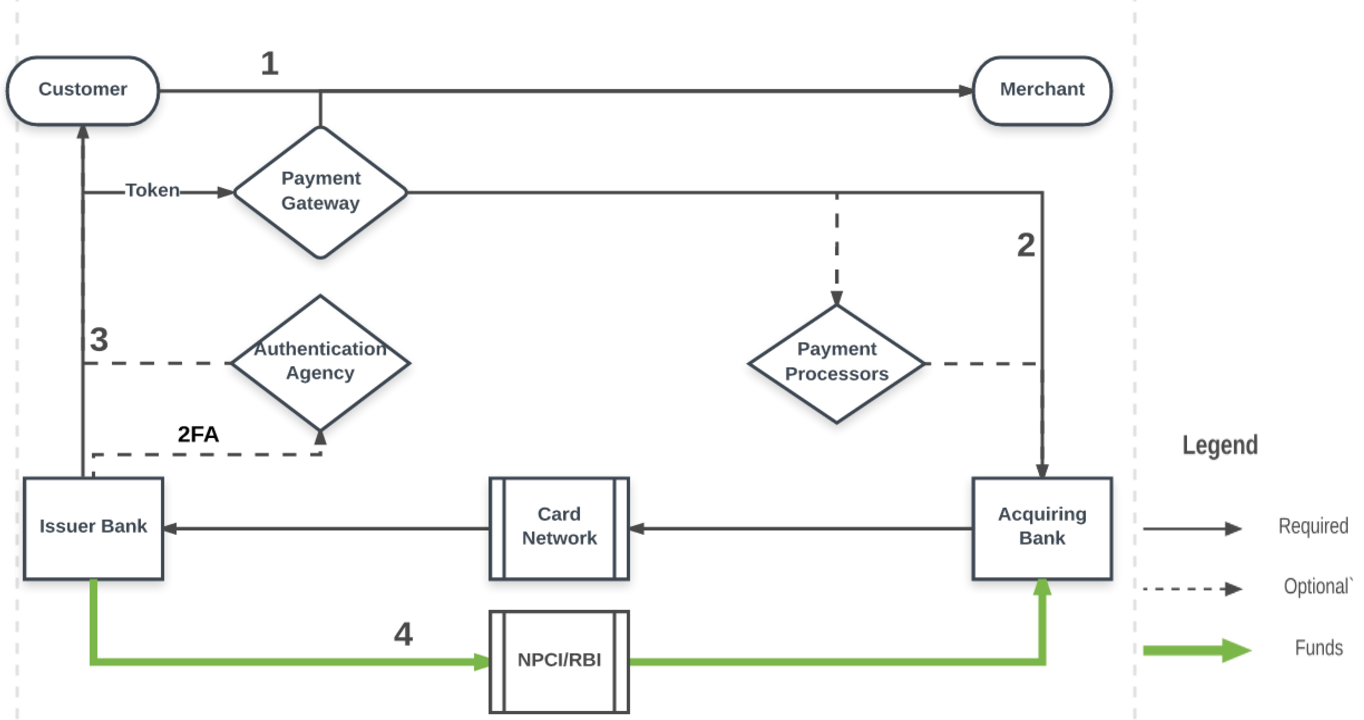

The FFI’s focus to date has been understanding customer-level risks in digital finance. We wanted to use this opportunity to test our concerns with providers involved in payments transactions. To frame the discussion, and locate the various parties in the chain of a payments transaction, we presented a simplified schematic of our understanding of the payments ecosystem to the participants.

Figure 1: Card Not Present[1]: Online Payment Schematic

Source: The Future of Finance Initiative (2017)

The black arrows track transaction data flows and the green arrows tracking funds flows in the back end of a typical payments transaction. Participants agreed that this reflected the flows of a standard payments transaction. This schematic has remained broadly the same at the back-end for most forms of payments, but the challenges from the push towards newer forms of digital payment methods arise mainly due from (1) the variance among front-end customer-facing applications (2) increases in volumes of transactions and (3) the related data.

Pain Points include security, transaction failures and policy uncertainty

Discussions then followed through the afternoon about the operational aspects of completing payment transactions and pain points in the current scenario.

Data protection and data security: Payment services providers generally include clauses in their terms and conditions regarding customer data use. However the practices around this vary vastly. A key concern with direct impact on customers relates to data security, given the amount of data collected, stored and transmitted digitally in the payments process. ISO 27001 is the key global standard to which players in the payments industry generally aspire to. It was observed that full compliance with the standard was unaffordable for most providers, though the majority of them complied to the best extent possible.

Issues with the Payment Card Industry Data Security Standard (PCI DSS) — the industry standard for policies and procedures aimed at protecting data in card and payment transactions –- were also discussed. Adherence to all aspects of the PCI–DSS was patchy across industry participants. The standard does not have an enforcement body (being an industry standard with compliance driven by the requirements of other payment brands and acquirers). Concerns were raised that certain payment gateways and services were falling foul of the requirements without being censured –for example, by storing CVV for extensive periods of time in contravention of PCI-DSS.[2] It was pointed out that the PCI DSS provisions are from a pre-mobile era, and tend to be web-focussed. This results in gaps arising even in these standards with respect to data security for mobile transactions.

With regard to future regulation, participants stressed the need to balance the costs of compliance to be measured against evaluations of risk carefully when regulations are being formulated.

Hardware security: Hardware security is often overlooked in discussions around payments security. Participants discussed the absence of hardware checks for mobile phone handsets or regulations limiting pre-installed applications on mobile phones. This opens up the possibility of phones manufactured in other countries being sources of data theft and spyware. For instance, in 2016 firmware was found on Chinese manufactured smartphones being sold in the US which transmitted personally identifiable information (PII) to servers in China via a back door.[3]

To raise consumer awareness of security vulnerabilities and to drive providers to adopt better security practices, one idea suggested was to develop standardised indicators on apps and webpages to give users") an immediate indication of the level of security. An existing example of this is the green lock HTTPS URL marker (right) currently used to indicate that a web browser holds a Secure Socket Layer (SSL) certification.

an immediate indication of the level of security. An existing example of this is the green lock HTTPS URL marker (right) currently used to indicate that a web browser holds a Secure Socket Layer (SSL) certification.

Transaction failures and frauds: Participants noted that the payments industry needs to improve on the failure rates for transactions to avoid affecting consumer confidence and usage. There was consensus that the regulator could play a constructive role in publishing aggregated information about transaction failure rates to incentivise higher data security standards. Providers themselves would shy away from publishing this kind of data individually. However, aggregated data published by a neutral third party or regulator could drive the providers to measure themselves against this benchmark and aspire to better rates.

Regulatory uncertainty and intervention: Participants discussed concerns about the impact of regulatory uncertainty along with how prescriptive regulatory standards had the potential to stifle innovation. Providers were concerned about competing with Government sponsored payments products and services and were anxious about Government subsidies and price caps that could put pressure on market prices, and introduce uncertainty for providers who were seeking to be commercially viable. There was also discussion on the need for having a level-playing field for new payment service providers as against established providers like banks.

Overall, the workshop was a fascinating deep dive into the perspective of the various actors who participate in making a payment transaction possible – while keeping the customer’s experience and concerns at the heart of the discussions.

—-

About the Future of Finance Initiative:

The Future of Finance Initiative (FFI) is housed within IFMR Finance Foundation and aims to promote policy and regulatory strategies that protect citizens accessing finance given the sweeping changes that are reshaping retail financial services in India – including those driven by Indiastack, Payments Banks, mobile usage and the growing P2P market.

—

[1] Card not present (CNP) refers to a purchase a consumer makes without physically being present or presenting his or her credit or debit card at the time of purchase. CNP transactions often occur online and are conducted by consumers without the actual in-store credit card swipe – which is likely the major direction of travel, as more digital payments are made over mobile/internet to pay for goods and services.

[2] For more see: https://www.pcisecuritystandards.org/pdfs/pci_fs_data_storage.pdf

[3] For more see: http://gadgets.ndtv.com/mobiles/news/chinese-firm-installed-back-door-on-thousands-of-smartphones-says-it-was-a-mistake-1626136

One Response

Awesome article and very informative! Thank you!