Payments banks (PBs) were established by RBI in 2014, making them the first truly differentiated type of bank in India, as they are authorised to perform only the banking functions of providing deposits (of balances up to Rs. 1 lakh) and payments/remittances. The concept of payments banks was introduced in 2014 in the report of the RBI Committee on Comprehensive Financial Services for Small Businesses and Low-Income Households (CCFS) chaired by Dr. Nachiket Mor[1]. PBs were set up with the objective of ‘providing small savings accounts and payments/remittance services for the underserved, such as low-income households, small businesses, migrant labour workforce and other users.’ The real value from the PB model has been envisaged to be coming from enabling cash-in cash-out (CICO) services in unbanked locations where cash will continue to dominate for a reasonable time. This cash-out feature sets them apart from the Pre-Paid Instrument (PPI) or wallet licenses which by design cannot provide the CICO service[2]. This restriction has however been relaxed to an extent by the RBI since then[3].

We at Dvara Research studied the performance of the four fully operational PBs – Airtel Payments Bank, India Post Payments Bank (IPPB), Fino Payments Bank and Paytm Payments Bank, to assess whether they have moved the needle on the goal of financial inclusion. We analyse the question of performance from the point of

- whether there has been a proliferation of transaction touchpoints due to PBs (not just branch and Business Correspondents (BC) touchpoints but also ATMs and POS as well as by significantly increasing touchpoints in unbanked rural centres), and

- whether there is a difference in the nature of transactions enabled by PBs versus those enabled by full-service banks through physical touchpoints and purely digital modes.

Following are the major findings:

With the establishment of PBs, there has been a proliferation of touchpoints, of largely the non-branch type

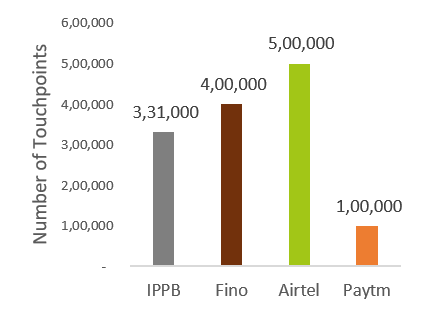

True to form, the PBs set up a vast network of touchpoints, aided largely by the established nature of some of their parent companies. Airtel PB, with the current largest touchpoint network, has the potential to widen its network further by leveraging its parent’s existing network of more than 10 lakh retailers[4]. Another instance of inherited advantage is of IPPB, which enabled about 88% of India Post’s post offices and equipped more than 80% of their postmen to provide payments bank services. IPPB stands out with the largest number of branches – one for each district, ensuring a cross country coverage, including in the rural areas.

Figure 1- Total Number of PB Touchpoints

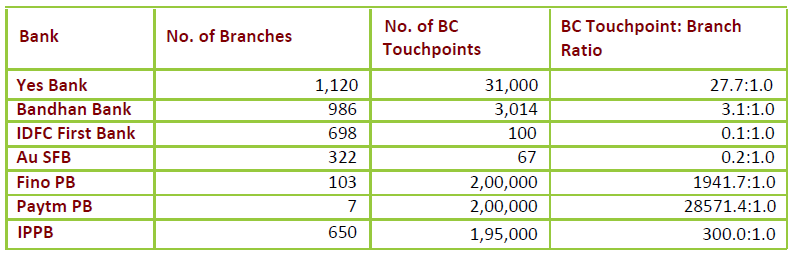

Table 1- BC Touchpoint: Branch Ratio

We see that in comparison to full-service banks, PBs have quite a different operating model, engaging with a much larger proportion of agent network. The PB model can function more effectively by widening their network further with a variety of partnerships as demonstrated by Fino PB working together with Rajasthan state government and Bharat Petroleum[5],[6]. That PBs have such a vast network of touchpoints is beneficial to the full-service banks too who can employ the PBs as BCs to serve in regions which were hitherto considered unviable for branch-based operations.

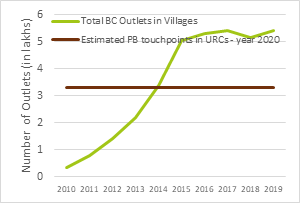

Given that the branch authorisation policy[7] requires 25% of a bank’s banking outlets to be in unbanked rural centres (URCs), the large network of PB touchpoints have an additional benefit that potentially 3 lakh touchpoints now provide access to payments services in unbanked areas. To put this into perspective, as of March 2019, there are 5.4 lakh BC touchpoints in villages as reported by RBI[8] for a total of about 6.4 lakh villages (as per Census 2011).

Figure 2- Number of BC village points vs PB URC touchpoints

PBs facilitated high volumes of digital transactions but was it ‘inclusive’ enough?

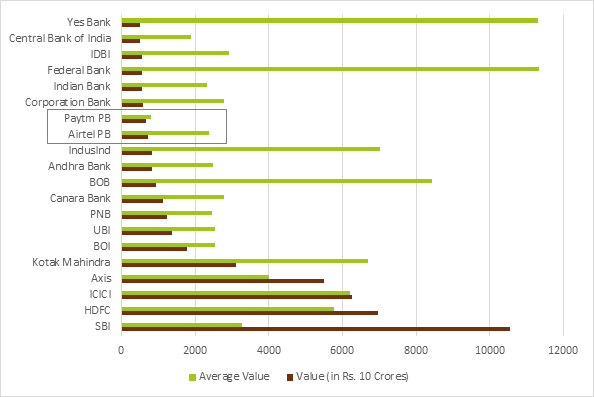

PBs, particularly Paytm PB, facilitated large volumes of digital transactions, outperforming most of the full-service banks. Compared to 20 Scheduled Commercial Banks (SCB) with the highest value of mobile transactions in March 2020, Paytm PB had the lowest average mobile transaction values[9] (see Figure 3). The low-ticket size of Paytm PB’s average transaction clearly points to an operating model different from full-service banks. However, this may simply be due to its payments model and not really a testament to fulfilling the objective of serving the underserved. IPPB too stands out with its high value of average mobile transaction[10] (relative to other PBs), despite having both low totals of both volume and value of transactions, suggesting a model focusing away from small-ticket transactions by underserved/rural customers.

Figure 3 – Average Mobile Transaction Value of Banks with the Highest Value of Mobile Transactions – March 2020[11]

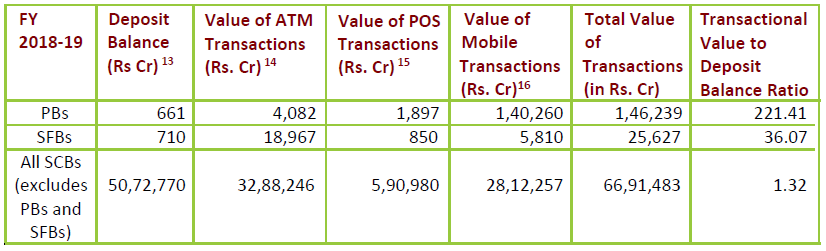

PB accounts were used largely for payments, and not for savings

To estimate the usage of PBs’ accounts in comparison to those of other bank groups, we present below a ‘transactional value to deposit balance ratio’[12], a measure of ‘velocity’ of deposits.

Table 2- Transactional Value to Deposit Balance Ratios of different Bank Groups

We see from the very high value of the ratio that there was considerable achievement of the primary objective of PB accounts to facilitate payments. This allows them to function as providers of transaction-accounts to complement full-service banks which cater to, among others, the provision of bank accounts and term deposits for the purpose of savings.

In our report, we also discuss the nature of competition from SCBs and Prepaid Instrument Providers (PPI) that PBs have had to face. PBs have also had to establish their presence within a very rapidly evolving and uncertain regulatory landscape as well as face new and unforeseen challenges such as the introduction of Unified Payment Interface (UPI), the continuation of the PPI model, and most recently permissions to cash-out from wallet providers at various physical locations (up to Rs.2000).

We conclude that with the establishment of PBs, there has been a proliferation of touchpoints, of largely the non-branch type. There is evidence of large aggregate numbers attributable to the PBs in case of networks, especially due to Airtel PB, or in transaction volumes, especially due to Paytm PB. PBs have facilitated high volumes of digital transactions, but it cannot be concluded whether these were ‘inclusive’ enough. For instance, were PBs able to provide safe transactions infrastructure in regions that banks find hard to service, for instance in Left Wing Extremism (LWE) districts? It can be concluded strongly that PB accounts were used largely for payments, and not for savings. However, due to lack of data, it is difficult to conclude whether PB touchpoints have indeed been opened in previously unbanked or underbanked locations and whether digital and physical transactions emanated from these locations because of the presence of a PB touchpoint.

Considering that there have been many changes in the financial sector space since the introduction of PB licensing by RBI, it remains to be seen how PBs would emerge successful given their limited functionality and strong competition from other players such as PPIs.

To know more, please read our report on “Tracking Performance of Payments Banks against Financial Inclusion Goals” here.

[1] Committee on Comprehensive Financial Services for Small Businesses and Low Income Households Report available at: https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/CFS070114RFL.pdf

[2] The Banking Regulation Act defines banking to mean “the accepting, for the purpose of lending or investment, of deposits of money from the public, repayable on demand or otherwise, and withdrawal by cheque, draft, order or otherwise”. A strict reading of this definition would mean that any withdrawal in a financial form, even into a bank account (as with PPI wallets) could be construed as a deposit and hence any transaction that allows for financial value in and financial value out, rather than financial value in and goods and services out, could be construed to be a deposit.

[3] e-Wallets have now been given permissions by RBI to withdraw up to Rs. 1000 per day in Tier 1 and 2 locations, and up to Rs. 2000 per day in Tier 3 and above locations. This is possible at specific merchant locations. The wallet holder transfers funds for ‘cash-out’ to the UPI-Id of the merchant who then disburses cash to the wallet holder.

[4] ‘Our business and value creation model’, Bharti Airtel Annual Report – FY 2018-19, Accessed from https://assets.airtel.in/static-assets/cms/Bharti-Airtel-Limited-Integrated-Report-Annual-Financial-Statements-2018-19.pdf

[5] https://www.finobank.com/about-us/news-media/press-release/2016/fino-paytech-in-a-strategic-partnership-with-bpcl-for-its-payments-bank-foray/#:~:text=Mumbai%2C%20July%2029%2C%202016%3A,Petroleum%20Corporation%20Limited%20(BPCL)

[6] https://www.finobank.com/about-us/news-media/press-release/2017/fino-payments-bank-signs-up-e-mitra-as-bc-points-in-rajashtan/

[7] Rationalisation of Branch Authorization Policy – Revised Guidelines, RBI Notification, May 18, 2017. Available at: https://rbidocs.rbi.org.in/rdocs/notification/PDFs/NOTI3062319C9C94C33494794C2B5271CF92878.PDF

[8] Table IV.6: Financial Inclusion Plan: A Progress Report, Credit Delivery and Financial Inclusion, RBI Annual Report 2018-19. Available at: https://m.rbi.org.in/Scripts/AnnualReportPublications.aspx?Id=1259

[9] Paytm PB’s average mobile transaction value for March 2020 was around Rs. 807. The average value of mobile transactions for the SCBs with the top 20 most valued transactions was around Rs. 4495 in the same period.

[10] IPPB’s average value of mobile transaction in March 2020 was Rs. 6762. Source: Bankwise volumes in ECS/NEFT/RTGS/Mobile Transactions – March 2020, RBI Data. Available at: https://www.rbi.org.in/Scripts/NEFTView.aspx

[11] Calculated from: Bankwise volumes in ECS/NEFT/RTGS/Mobile Transactions – March 2020, RBI Data. Available at: https://www.rbi.org.in/Scripts/NEFTView.aspx

[12] To obtain transactional value, the value of physical (at ATMs and POS) and mobile transactions using debit cards (where the bank was the issuer) was added up to obtain a reasonably complete picture of total value of transactions emanating from debit cards (a proxy for bank accounts) without overlap of numbers across modes and channels of transactions. The data for mobile transactions excludes those transactions that were initiated through non-mobile internet-enabled platforms (such as internet banking), and those initiated at branches of banks (such as deposit and withdrawal transactions at the teller).

[13] The deposit amount for SFBs and SCBs represents the amount present in current and savings accounts. In both these cases, the term deposit amount has been excluded to aid an appropriate comparison to the PBs’ amount. Deposit amount is the average of values outstanding as of March 2018 and March 2019.

[14] The value of ATM transactions is of those performed by the debit cards issued by the bank/bank-group at ATMs in April 2018 to March 2019.

[15] The value of POS transactions is of those performed by the debit cards issued by the bank/bank-group POS terminals in April 2018 to March 2019.

[16] The value of mobile transactions are of those individual and corporate payments initiated, processed and authorised using a mobile device.