Nano-enterprises, despite being ubiquitous in both rural and urban India, face a double dilemma. First, they are not represented as a distinct category in the official enterprise classification of MSME Act and gets subsumed within the larger category of micro-enterprises. Although there exists some overlap between the two categories, there is considerable difference in the scale and operational realities of the two[1]. Secondly, the largely informal nature of nano-enterprises means that they often lack sufficient documentation to avail any formal credit – to be used either for growing their business or for working capital needs. This has led to the vast majority of nano-enterprises in India remaining at a subsistence level in their operations. Consequently, India’s MSME sector is dominated by large number of small firms, a limited number of large firms, and very few medium sized firms in between (the so called ‘missing middle’)[2].

Access to suitable credit could enable growth-oriented nano-enterprises to invest in productive assets, adopt new technologies, smooth working capital cycles, and expand their scale of operations. By easing financial constraints, such credit can help viable enterprises transition from subsistence activities to growth-oriented businesses. Against this backdrop, estimating the market size for nano-enterprise credit offers valuable insights. Understanding the potential size of the credit market for nano-enterprises provides an indication of the growth opportunities available to commercial lenders seeking to expand their portfolios. Furthermore, it serves as a useful benchmark for policymakers to assess supply side credit interventions by quantifying the gap between the potential demand for credit and its current supply.

Previous Estimates of Small Enterprise Credit Access

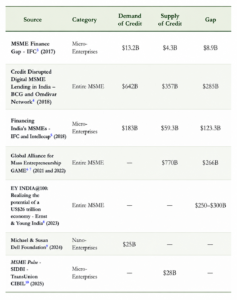

We surveyed major reports and industry publications published over the last decade that have attempted to quantify the size of the credit market across various MSME segments in India. It should be noted that, with the exception of the Michael & Susan Dell Foundation, none of the others view nano-enterprises as a distinct category. A summary of the same has been provided in Table 1.

Table1: Previous Credit Market Estimates for MSMEs in India

Note 1: Arranged in order of year of publication

Note 2: Only MSME Finance Gap, Financing India’s MSMEs and SIDBI – TransUnion CIBIL reports have methodology elaborated in their reports

The most frequently cited report in the table is “Financing India’s MSMEs”, published by the International Finance Corporation (IFC) and Intellecap in 2018. The report recognizes the heterogeneous financing needs of enterprises of different sizes and provides estimates for addressable credit demand. By benchmarking this demand with the available supply of credit, the report estimates a credit gap of $123.3 billion for Indian micro-enterprises. In a similar vein, the “MSME Finance Gap” report published by the IFC a year earlier (2017) had estimated a much smaller credit gap of $8.9 billion. The difference stems primarily from its narrower coverage, as the latter’s estimate was derived using data on only 889,000 registered micro-enterprises from the Fourth All India Census of MSMEs (2006–07), compared with the estimated universe of 5.29 crore micro-enterprises considered in the former. Nevertheless, the estimates reported in “Financing India’s MSMEs” are themselves now nearly a decade old. Since then, both the number of enterprises and their demand for credit have changed substantially, limiting the relevance of these figures for understanding the current landscape.

The underlying methodologies are not described in detail for the other sources listed in the table. Moreover, the SIDBI–TransUnion CIBIL (2025) report presents only credit supply figures and uses a different classification framework for micro-enterprises altogether. Hence, we refrain from undertaking any cross-comparison of the estimated figures provided.

Computing Market Size for Nano-enterprise Credit: Dvara Research Estimates

To calculate the market size for credit, we employ a simple formula of

Market Size = Number of Nano-enterprises × Average Loan Size.

In order to estimate the number of nano-enterprises in India, we use data from the Annual Survey of Unincorporated Sector Enterprises (ASUSE), a nationally representative survey conducted annually by the National Sample Survey Office (NSSO) since 2021. ASUSE captures non-agricultural unincorporated enterprises and provides nationally representative, unit-level data on ownership, employment, location of operation, production, turnover, assets and liabilities, access to credit, digital usage, formal registration etc. Based on turnover data from ASUSE 2023-24, we estimate that there are approximately 7.3 crore nano-enterprises in India[11]. Of these nearly 88% are Own Account Enterprises (OAE) or businesses that operate without any hired workers while the rest are Hired Worker Establishments (HWE). It should be noted that the majority of HWEs and OAEs remain concentrated at the lower end of the turnover distribution, with 72% and 98% respectively, having an annual turnover of less than 25 lakhs [12].

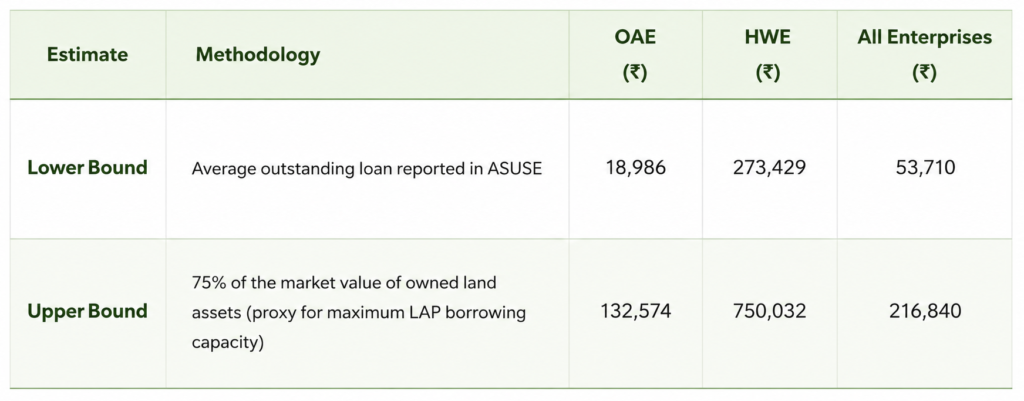

Further, we extrapolate a lower and upper limit for the average ticket size of a nano-enterprise loan. For the lower-bound estimate, we use the average outstanding loan reported in the ASUSE data. For the upper-bound estimate, we calculate the maximum potential borrowing capacity of an enterprise based on the value of the land assets it owns, reflecting the lending approach adopted by emerging micro loan-against-property (LAP) products. To ensure a conservative range, we assume a maximum loan-to-value (LTV) ratio of 75 percent[13].

Table 2. Methodology for estimating ticket size of nano-enterprise credit

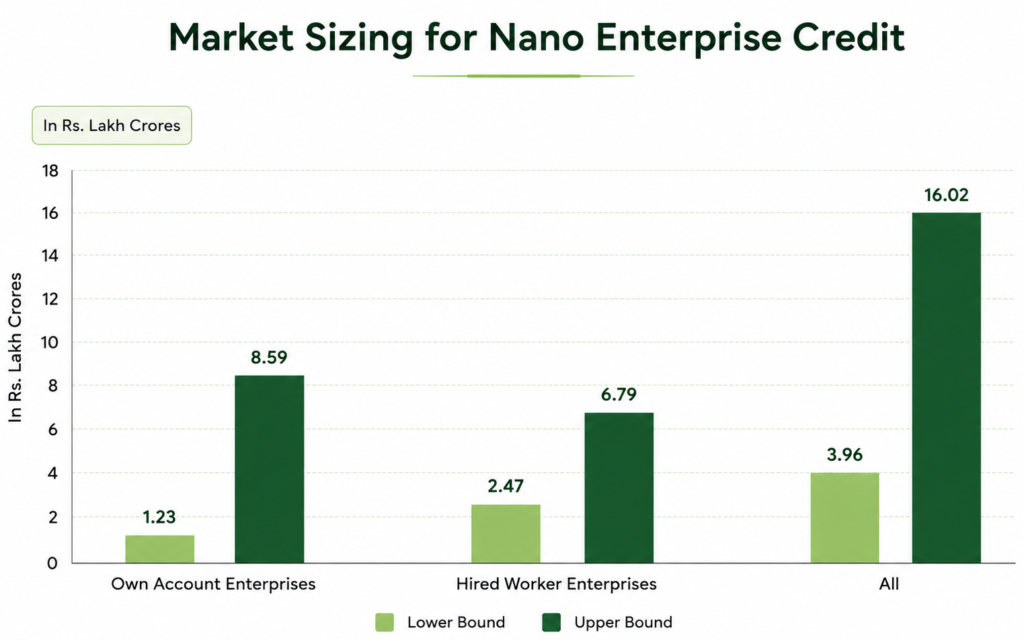

Figure 1: Upper and lower bound estimates for nano-enterprise segment.

Subsequently, we estimate the total potential credit market for nano-enterprises in India to lie between ₹3.9 lakh crore ($44 billion) and ₹16 lakh crore ($178 billion)[14]. Given their growth impetus, HWEs represent the ideal target market for credit expansion with a potential market size ranging between ₹2.4 lakh crore ($26 billion) and ₹6.7 lakh crore ($76 billion).

These estimates should be interpreted with caution. They represent the total potential credit capacity of the sector rather than its addressable credit demand. Not all nano-enterprises may need credit, and their credit needs are likely to vary significantly depending on enterprise characteristics. Additionally, high volatility within the sector means that a non-trivial number of these enterprises shut shop within their first year of operations. Hence, we do not attempt to estimate any credit gap by comparing these figures with the current supply of credit, as doing so would risk overstating the unmet demand for credit.

Conclusion

We believe the estimates to be indicative of the opportunity cost of failing to unlock the growth potential of India’s nano-enterprises.For commercial lenders, this segment represents a new avenue of growth, where expanded access to credit could yield substantial development gains as well. For policymakers, the estimates highlight the scale of the economic opportunity linked with enabling nano-enterprises to expand and become more productive. As the largest segment, in numbers, of India’s enterprise landscape, nano-enterprises remain central to the country’s growth story.

_________________________________________________________________________________________

Footnotes

[1] Financial Express. “How Nano Enterprises Are Defined in India? Check Criteria.” 2024. https://www.financialexpress.com/business/sme/how-nano-enterprises-are-defined-in-india-check-criteria/3609552/

[2] Krueger, Anne O. The Missing Middle. Working Paper No. 230. Indian Council for Research on International Economic Relations (ICRIER), 2009. https://www.econstor.eu/handle/10419/176248

[3] International Finance Corporation. MSME Finance Gap. Washington, DC, 2017. https://doi.org/10.1596/28881

[4] Tripathi, Saurabh, Amit Kumar, Manoj Ramachandran, et al. Credit Disrupted: Digital MSME Lending in India. Boston Consulting Group & Omidyar Network , 2018. https://www.bcg.com/credit-disrupted-digital-msme-lending-in-india

[5] Financing India’s MSMEs – Estimation of Debt Requirement of MSMEs in India. International Finance Corporation & Intellecap, 2019. https://www.ifc.org/en/insights-reports/2019/financing-indias-msmes-estimation-of-debt-requirement-of-msmes-in-india

[6] Unlocking Credit for India’s Job Creators. Global Alliance for Mass Entrepreneurship (GAME) , 2021. https://massentrepreneurship.org/wp-content/uploads/2023/01/GAME-Report_Unlocking-Credit-for-Indias-Job-Creators.pdf

[7] Global Alliance for Mass Entrepreneurship (GAME) Annual Report 2022. 2022. https://massentrepreneurship.org/wp-content/uploads/2026/04/GAME-Annual-Report-2022.pdf.pdf

[8] Ernst & Young. “India@100: Enabling $26 Trillion Economy.” 2023. https://www.ey.com/en_in/insights/india-at-100

[9] Goyal, Rakesh. “Enabling the Growth of Nano Entrepreneurs Through Customized Credit Solutions.” Michael & Susan Dell Foundation, June 26, 2024. https://www.dell.org/ideas/growing-indias-nano-enterprises/

[10] MSME Pulse Special Edition – June 2025. Small Industries Development Bank of India & TransUnion CIBIL, 2025. https://www.sidbi.in/head/uploads/msmepluse_documents/MSME_Pulse_Special_Edition_Report_june_2025.pdf

[11] We define nano-enterprises as those firms whose annual turnover is less than ₹1 Crore. One can find the number of same from ASUSE data where, Turnover for a firm=∑Total Receipts−∑Own-Account Consumption.

[12] H S, Shreenandan, and Navaneeth M S. “Mapping India’s Informal Enterprises: A Descriptive View from ASUSE.” Dvara Research, March 13, 2026. https://dvararesearch.com/mapping-indias-informal-enterprises-a-descriptive-view-from-asuse/

[13] Lakra, Pallavi. “What Is LTV in the Case of LAP? How Is It Determined?” Poonawalla Fincorp, 2024. https://poonawallafincorp.com/blogs/loan-against-property/what-is-importance-of-loan-to-value-ratio-in-lap

[14] US $1 = ₹90