A recent paper titled ‘Searching for Fish in Trees (緣木求魚)? Economic Development when Context Matters’ (hereafter referred to as Moscona et al., 2026)[1] by three economists arrives at a modest conclusion that much of development research and policymaking rests on fragile assumptions about the manipulability of human behaviour and the universality of what is good and bad for economic development. The authors argue that these assumptions, when fed into the design of policy interventions, may generate unintended or adverse consequences, thereby underscoring the urgent need to engage in a deep study of the local context and population to design thoughtful interventions.

The paper builds its arguments by developing a framework for analysing the determinants of economic development and their implications for policy. In doing so, they distinguish between classical determinants—such as inputs into education and health, access to credit, and geography—and non-classical determinants—such as cultural values, social norms, beliefs, identity, and social organization. They classify these determinants along two policy-relevant dimensions: whether they can be clearly ranked in terms of their contribution to development (vertical versus horizontal) and whether they can be directly altered through policy intervention (manipulable versus non-manipulable). Through a meticulous literature review, the authors demonstrate that policy impacts are often hard to predict and are mediated by local social and cultural context. They argue that non-classical determinants are even more complicated to change through policy interventions and more difficult to rank in welfare terms. They posit that traits commonly viewed as obstacles to development may be well adapted to local conditions or even supportive of economic performance, a possibility they refer to as ‘reverse vertical’.[2]

In this blog, I apply this framework to the context of financial inclusion, a development goal that has attracted significant attention globally for over decades now. My objective in doing so is to pause and reflect on the collective effort that has gone into accelerating financial inclusion, with a view to understanding the kinds of interventions that have largely been successful versus those that haven’t and the underlying reasons for the same. I begin by asking- what are the determinants of financial inclusion, and use the framework developed by Moscona et al., 2026 to answer this question.

What are the Determinants of Financial Inclusion?

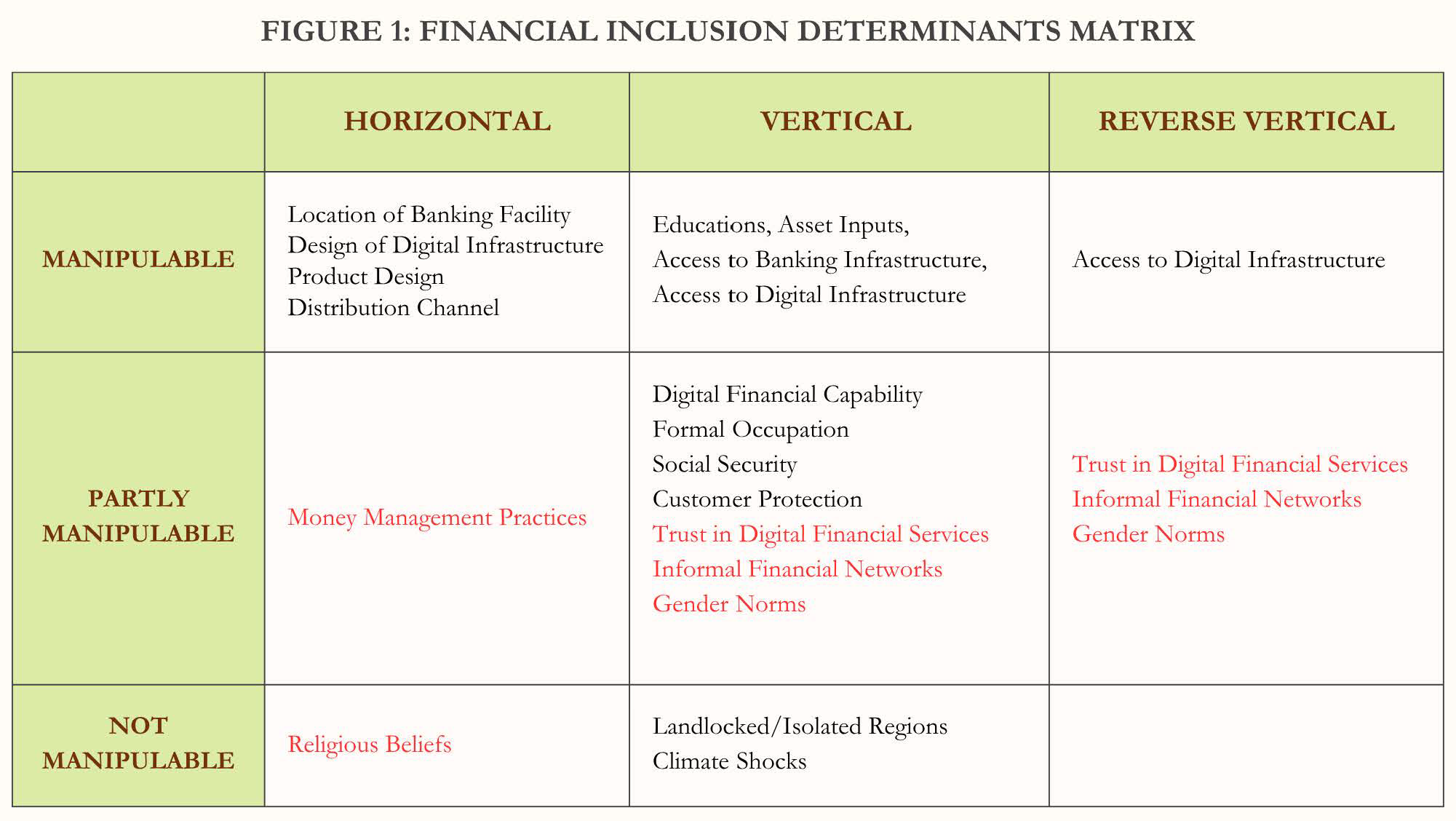

Figure 1[3] displays the matrix of determinants of financial inclusion. By financial inclusion, I mean access to a suite of formal financial products and services, at an affordable cost, delivered in a fair and transparent manner. Vertical determinants are those that can be reasonably ranked in welfare terms, and Horizontal determinants are those that cannot be. In other words, while vertical determinants imply a clear policy direction, horizontal determinants do not imply a universally optimal model, and its impact on the desired outcome varies by context. Reverse Vertical determinants allow for the possibility that certain determinants that are often perceived as negative can actually be positive (and vice versa). Manipulable determinants are those that can be changed through policy or development intervention, and non-manipulable determinants are those that cannot be. Partly Manipulable determinants are those that are difficult to change through policy or development interventions, largely because of the role classical determinants plays in mediating or undermining these interventions. Determinants marked in black are classical determinants, whereas those marked in red are non-classical determinants.

In the following sections, I describe the contents of each cell and explain their positioning. In doing so, I have deliberately avoided adding citations, particularly for those research findings that are well known.

- Vertical, Manipulable

Vertical and manipulable determinants of financial inclusion are those that have a clear ranking and can be affected directly through interventions. Access to banking infrastructure in the form of physical bank branches and proximity to agent networks is one such determinant that has universally led to greater financial inclusion. Similarly, digital infrastructure in the form of digital ids, digital public infrastructure that enables large-scale cash transfers, creation of interoperable payment systems, and data exchange platforms are all positive determinants of financial inclusion. Individual characteristics such as higher levels of education and higher levels of asset ownership are known to positively correlate with financial inclusion. At the same time, these determinants can be manipulated through asset transfer and public schooling programs on the demand side, and through the development of necessary financial and digital infrastructure on the supply side.

- Vertical, Partly Manipulable

Determinants of financial inclusion, such as digital financial capability and formal occupation, are also vertical determinants, in the sense that those with higher levels of digital financial capabilities and those engaged in formal occupation are more likely to be financially included. However, these are only partly manipulable, given their multidimensionality. Take, for example, the occupational choice of an individual in a low-income household setting- the occupation choice of a primary income earner is influenced by their family’s initial endowment levels, historic occupational choices, social network, the socio-cultural context they find themselves in, and their own individual proclivities. In this scenario, while government programs can promote livelihood training and skill development programs, whether these interventions yield the desired outcomes will depend on the interaction of these multiple factors and may not always lead to an increase in formal employment. Similarly, while access to affordable social security can be made available through subsidised insurance and pension accounts, adoption and sustained engagement is often influenced by their socio, economic, and cultural context, and therefore are only partly manipulable. Customer protection too falls in this cell as greater customer protection always leads to more meaningful financial inclusion, but the ability to, in reality, translate customer protection policies into customer centric practices among financial service providers is often challenging. (We will discuss the non-classical determinants marked in red in this cell when discussing the scenario of Reverse Vertical.)

- Vertical, Not Manipulable

Geographical factors such as residing in isolated regions and being exposed to climate shocks are associated with weaker financial inclusion and therefore constitute vertical, not-manipulable determinants.

- Horizontal, Manipulable

Horizontal and manipulable determinants of financial inclusion are those where it is not possible to rank the determinants, but that can be affected directly through interventions. Examples of these determinants are aspects such as the appropriate location of banking infrastructure or the suitable design of digital infrastructure to serve the intended population. Similarly, the design and distribution channel through which an FSP offers its services is also context-specific and is tailored to suit the needs of its customers. No universal model exists in relation to these determinants. Moreover, these determinants can easily be manipulated (relatively speaking) through deliberate supply-side efforts.

- Horizontal, Partially Manipulable

Money management practices are categorised as a non-classical determinant. These practices vary across cultural contexts and have a bearing on households’ level of engagement with formal finance. Indian households, for example, save and invest primarily in gold and physical assets, lowering their likelihood of engagement with formal financial assets. Similarly, in low-income settings, borrowing and lending within closed social networks is used as a strategy for managing shocks and raising lumpsums. These practices are anchored in local socio-cultural norms which are often difficult, though not impossible, to manipulate.

- Horizontal, Not Manipulable

Religious beliefs are often rooted in deep historical values that are hard to change and therefore feature under this category, as a non-classical determinant. For example, one of the central principles of Islamic finance is the prohibition of interest, due to which many Muslims may avoid conventional banking products that charge or pay interest. While there is no single universal association between religious beliefs and financial inclusion, households from different faith might be influenced in their financial behaviour differently.

- Reverse Vertical

Finally, we discuss determinants that are typically classified as vertical determinants of financial inclusion, but that may need repositioning.

In terms of classical determinant access to digital infrastructure is often treated as a vertical determinant- more digitisation is assumed to be better. However, literature also points to issues of the digital divide, exclusion through mandatory digitisation, and fear of digital systems. These determinants are often manipulable through top-down interventions but can sometimes lead to negative unintended consequences.

In terms of non-classical determinants, all three determinants laid out in Figure 1, fall in the Partly Manipulable category as policy interventions can influence change, albeit slowly and sometimes even adversely. Below, we discuss these three determinants briefly.

First, trust in Digital Financial Services (DFS) is seen as a vertical determinant, as a lack of trust is seen as an impediment to financial inclusion. While it is true that some level of trust in DFS is essential to use formal financial instruments, too much trust, especially in DFS, can be dangerous. Research shows that excessive trust can increase vulnerability to digital debt traps as digital platforms reduce friction and trusted apps normalise borrowing. This becomes salient in contexts where digital financial capabilities are relatively low. Strong trust in digital systems can create complacency around fraud, data privacy, predatory practices, algorithmic decision making. Our own study at Dvara Research[4] shows that high trust in digital platforms may increase susceptibility to digital fraud. Therefore, when high levels of trust in DFS should be classified as vertical and when as reverse vertical depends on the context, the target group, the regulatory environment, and so on.

Second, participation in informal financial networks is typically perceived negatively, as it may reduce exposure to external financial institutions and therefore, appears as a vertical determinant. However, here the source of reverse vertical is the difference in outcome relevance. While informal financial networks are often viewed through a lens of creating exclusionary effects, the purpose it serves in the lives of households, especially those who are low-income, is that of survival under conditions of radical uncertainty. Maintaining and strengthening social capital with closed-knit groups is therefore a deeply valued cultural norm.[5]

Third, literature on women’s financial inclusion positions gender norms as barriers to their inclusion. Therefore, removing gender norms is perceived to improve women’s participation in and engagement with formal financial systems. Here, however, the source of reverse vertical is that local context matters.[6] Firstly, research shows that in some contexts, existing gender norms indeed facilitate rather than hinder financial inclusion. Secondly, when gender norms do not align with financial inclusion priorities, rather than attempting to change aspects of social and cultural structure (trait-making approach), it might be more effective to adapt policy design to the local context (trait-taking approach), as demonstrated by Moscona et al (2026). This could mean, for instance, designing financial products and services for women based on their intra-household roles and responsibilities. If this entail money management in the form of managing household budgets, juggling debt, building relational savings, then any product/service that helps women manage these responsibilities effectively could have a better chance of increasing their levels of engagement with formal finance.

Closing Reflections

In this blog, I have attempted to summarise the vast literature on the determinants of financial inclusion using a framework developed by Moscona et al (2026). As development researchers, working on action research projects in collaboration with donors, policymakers, financial service providers, and other stakeholders, undertaking this exercise is a useful reminder of the position we hold in influencing the discourse and the lived realities of low-income households whose lives we hope to improve through our research. My aim with this blog is to inspire other development researchers and policymakers to pause and reflect on questions, problem definitions, and solution approaches with a view to answering for themselves key foundational questions before designing interventions. These foundational questions can take the following shape-

- What outcomes am I seeking to change through the intervention, and why? Are these outcomes manipulable? Why or why not?

- Are these outcomes well adapted to local conditions?

- Does the intervention follow a trait-taking or a trait-making approach?

- Will the intervention give rise to any unintended consequences?

Footnotes

[1] Jacob Moscona, Nathan Nunn, and James A. Robinson, “Searching for Fish in Trees (緣木求魚)? Economic Development when Context Matters,” NBER Working Paper 34810 (2026), https://doi.org/10.3386/w34810.

[2] The contents of this paragraph have been heavily borrowed from the abstract of Moscona et al., 2026.

[3] The description of this figure is borrowed from Moscona et al., 2026.

[4] Are fraud awareness campaigns effective? (Dvara Research)- https://dvararesearch.com/wp-content/uploads/2025/05/Are-Fraud-awareness-Campaigns-Effective_Policy-Brief.pdf; The making of trust (Dvara Research)- https://dvararesearch.com/the-making-of-trust/

[5] For a fuller discussion of this theme, refer to Dvara Research’s paper on ‘Understanding low-income households from a social capital perspective’- https://dvararesearch.com/understanding-low-income-households-from-a-social-capital-perspective/

[6] For a fuller discussion on this theme, refer to Dvara’s blog on ‘Examining ‘Gender Gap’ in Financial Inclusion in India using the Global Findex Database 2025’- https://dvararesearch.com/examining-gender-gap-in-financial-inclusion-in-india-using-the-global-findex-database-2025/