(This post is authored by the Future of Finance Team at the IFMR Finance Foundation).

In the first and second posts of this series on the three Future of Finance Initiative (FFI) workshops hosted in April, we focused on digital payments and digital credit respectively. This blog summarises the key insights from the third workshop on digital investments. The workshop was attended by providers with a strong digital interface from across the investments ecosystem in India. We thank the participants for their frank and open views presented at the discussions.

The retail investments landscape in India is currently in the process of being disintermediated with the operating model of traditional providers and associated intermediaries being relooked at by fintech players in this space. Given this background and realising the continuing need for high-quality investment products for rural low-income households, we wanted to understand:

- How are providers providing solutions relevant to new market segments?

- Where are the risks and vulnerabilities across the chain of the players and processes associated with making digital investments?

In doing so, we found ourselves asking the following questions of the curated group of participants:

- How are providers dealing with any issues around (a) segregation of investments advice and product sale, and (b) customer data protection?

- What are the operational pain points for providers which are either created by or can be solved by policy and regulation intervention?

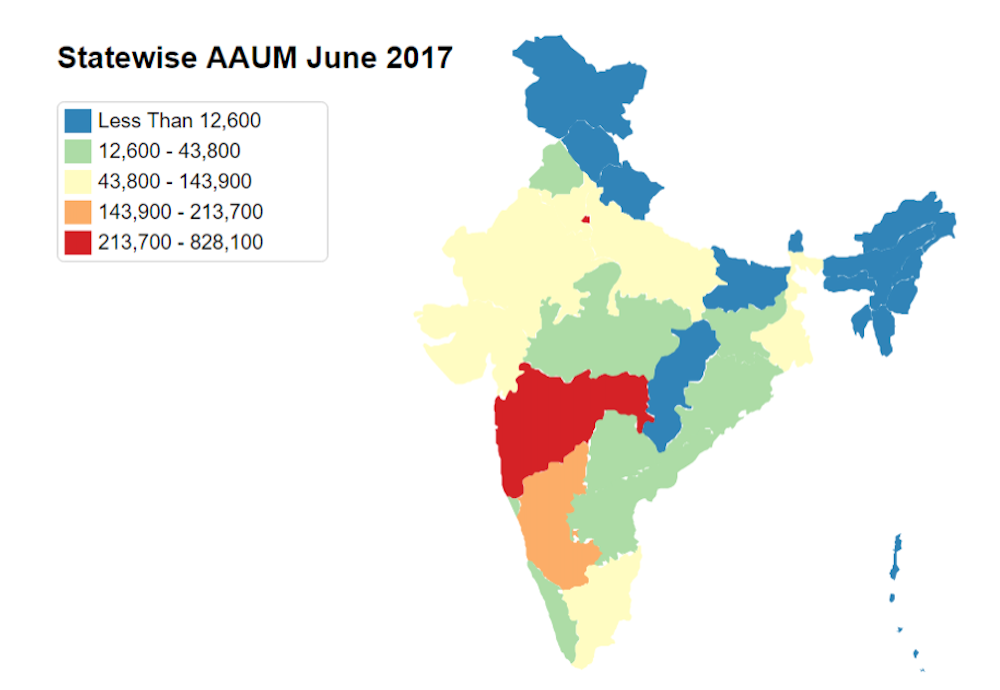

The first session at the workshop focussed on the current state of digital investments in India and was used to frame the discussion. An interesting visual from this discussion (reproduced below) was the geographic distribution of mutual funds sales in the country, which reveals that Western and Southern states have generated the majority of such investments. It was pointed out that in contrast, the penetration of life insurance is better in eastern parts of India. However, despite the growth of the mutual fund industry being significant in terms of absolute numbers, as a percentage of GDP, it is still estimated to be very low at 8.4% (as of 2016).[1]

Graphic: Geographic spread of mutual fund products (Source: Association of Mutual Funds in India) (Note: Legend in the graphic pertains to the average assets under management in Rs. crore)

Views on the future trends in the investments space and the role of regulation

Both offline and online consumer interfaces will continue to be critical: There was consensus among the participants that hybrid business models, incorporating both online and offline product distribution channels would prevail in the near future. It was however noted that there is a supporting environment in the form of digital public infrastructure (such as Aadhaar and India Stack) which has provided impetus for digital transactions in this space and that technology has enabled almost real time access to investments which was previously not the case.

The need for differentiated KYC processes: Some of the participants questioned the need for completing the full ‘know your customer’ process (including ‘in-person verification’) as a pre-requisite for investments in mutual funds since investor funds were moved from a KYC compliant bank account of the investor to the asset management company. One of the suggestions in this regard was to make full KYC a pre-requisite to redeem mutual fund investments and also put in place risk based KYC processes instead of uniform KYC processes irrespective of the nature and amount of investments.

On the role of industry standards and sector practices: The participants noted that there are currently no regulations regarding protection and security of an investor’s personal data which apply to entities operating in this sector. Some of the participants highlighted their internal best practices such as conducting vendor due diligence before sharing personal data and having robust data security protocols driven in part by shareholder requirements (especially for companies which have received venture capital funding).

On complaints mechanisms: The participants agreed on the need to strengthen grievance redressal mechanism to ensure better investor outcomes and suggested that investor awareness programmes (which are applicable to product manufacturers) be made outcome based, for instance by measuring the number of retail investors which take up mutual fund investments as a result of participating in or being exposed to awareness programmes. It should be noted in this regard that the Securities and Exchange Board of India (SEBI) currently requires depositories and asset management companies/registrar and transfer agencies to put in place ‘proper grievance redressal mechanism’ that is required to be communicated to the investors through the consolidated account statements.[2]

Role of agents and robo-advisory in the context of investment products

On treatment of advice and sale: Participants were keen to discuss the policy focus on separating advice and sale of investment products and commented that SEBI should consider regulating the quality of advice provided by agents. It should be noted that SEBI had recently put out a Consultation Paper on Amendments/Clarifications to the SEBI (Investment Advisers) Regulations, 2013 (available here) in this regard.

Some of the participants took a view that the current Indian market for portfolio advice is not at all data driven and potentially harmful advice is being provided to investors. It was also pointed out that the pass-through of commissions (received by insurance and mutual fund distributors) to investors is a rampant practice in India.

The promise of some of the new developments and digital investments is that more data flows can improve the range and quality of service in this space.

On considerations for robo-advisory services: The role of robo-advisory, i.e., providing financial advice with minimal human intervention, in investment advisory was also discussed. These advice algorithms could add value in terms of customising advice for consumers. There was recognition that training algorithm based investment advisory could retain the biases of human advisors which needed to be addressed in the long term and there were questions around the manner of selection of funds recommended by robo-advisors.

On disclosure: There was general consensus in the room that the onus should be on advisors to read offer documents and other disclosures and give informed advice to investors, instead of expecting potential investors to do so themselves.

—

About the Future of Finance Initiative:

The Future of Finance Initiative (FFI) is housed within IFMR Finance Foundation and aims to promote policy and regulatory strategies that protect citizens accessing finance given the sweeping changes that are reshaping retail financial services in India – including those driven by Indiastack, Payments Banks, mobile usage and the growing P2P market.

—

[1] Attributed to Mr. NK Prasad, President and CEO at Computer Age Management Services Private Limited. Please see MF investments rising in smaller towns: CAMS, The Tribune, 28 December 2016. Available at: http://www.tribuneindia.com/news/business/mf-investments-rising-in-smaller-towns-cams/342616.html.

[2] As per paragraph 14.3.2.8 of the SEBI Master Circular for Mutual Funds, 2016.