This blog examines the growth in household holdings of financial assets and liabilities for the period 2000-01 to 2016-17. For the purpose of this blog, financial assets refer to various saving and investment instruments held at formal financial institutions such as bank deposits, investments in debt securities, equities, mutual fund units, insurance and pension funds and small savings in addition to the currency issued by the Reserve Bank of India (RBI). Financial liabilities refer to liabilities in the form of loans and borrowings from commercial banks, cooperative non-credit societies, government and other financial institutions including non-banking financial companies (NBFCs). Using the data collated by the RBI as part of its 2019 Annual Handbook of Statistics on Indian Economy[1], we review the growth trends in financial assets and liabilities held by the Indian household sector[2]. Our motivation for this blog stems from analysing a new source of the supply side dataset that documents the growth across financial assets and liabilities compared to the demand side National Sample Survey Office (NSSO) dataset which is predominantly used to study the participation and allocation of Indian households in financial markets[3].

Research highlights significant benefits from participation and asset allocation in formal financial markets, leading to better household outcomes and improved household welfare (Campbell, 2006). The Household Finance Committee Report commissioned by the RBI in 2017 reported that a shift of a fraction of resources from physical assets to financial assets and a full replacement of non-institutional with institutional debt can lead to significant financial gains for Indian households. Similarly, research on macro assessment of the Indian household savings landscape highlighted financial assets to provide better liquidity and diversification options compared to physical assets, thereby facilitating efficient household lifecycle portfolio management (Badarinza et. al, 2016).

In the Indian context, financial inclusion broadly defined as ‘universal access to a wide range of formal financial services at a reasonable cost’ has been a policy priority for the Indian Government, given the extensive evidence on links between the efficient and extended financial sector and economic growth and development[4]. Efforts towards inclusive finance can be traced back to the post-independence period with a series of steps taken by the Government in bringing the unbanked and the undeserved within the ambit of formal financial system. RBI and the Government have taken several concrete steps towards increasing access to financial services across the country. The National Strategy for Financial Inclusion 2019-2024[5] is the most recent development in this regard, where the RBI has outlined key approaches to accelerate financial inclusion. Given this context and the increasing policy push towards accelerating access to formal financial services, we review the growth trends in formal financial market for the household sector over roughly the last two decades by examining the year on year instrument-wise growth across both financial assets and liabilities.

Financial Assets

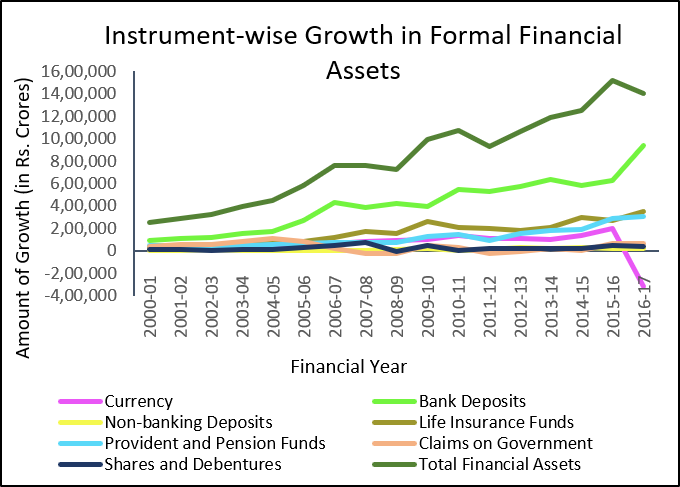

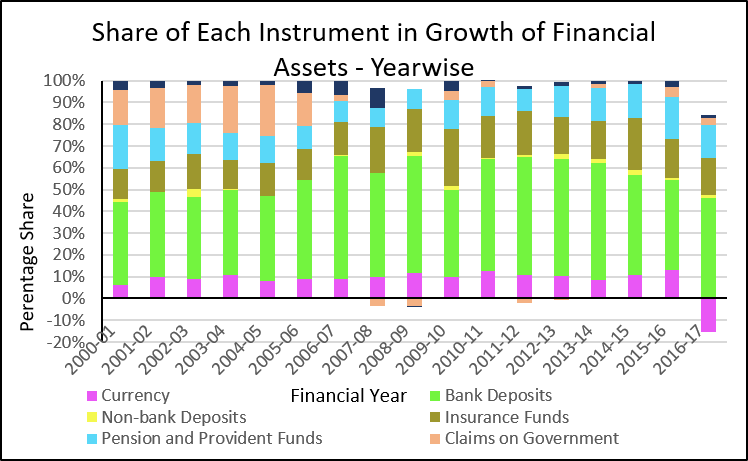

Households hold their financial assets in the form of currency, deposits, investments in debt securities, equities, mutual fund units, insurance and pension funds, and small savings. Graph 1A shows the growth in financial assets held by households across various instruments in the last two decades; Graph 1B captures the share of each instrument in the total growth of assets held by households, for each year in the analysis period.

Graph 1A: Instrument-wise growth in financial assets

Graph 1B: Share of each instrument in growth of financial assets

Financial asset holding of Indian households has consistently grown throughout the analysis period, at a CAGR of 18.59 per cent[6]. Deposits in commercial banks are the major drivers of growth in financial assets held, contributing over 48 per cent on an average to the growth in financial assets over the last two decades, followed much behind by life insurance funds (18 per cent), pension and provident funds (14 per cent), and currency (9 per cent). Other instruments like claims on government (7 per cent), shares and debentures (3 per cent), and deposits in non-bank financial institutions (1 per cent) have contributed to a considerably lesser degree to growth in assets held over the same period. Not surprisingly, we notice currency contributing negatively to growth in financial assets for the period 2016-17, owing to demonetisation. However, currency holdings of households reverted to normal levels in the subsequent quarters[7].

As observed, we don’t see a drastic change in the total share of bank deposits over time despite an increase in the ownership of bank accounts as a result of the Pradhan Mantri Jan Dhan Yojana (PMJDY), potentially reflecting a lack of an increase in the usage of bank accounts. The 2017 Global Findex Survey highlighted similar concerns, with non-usage of bank accounts at 48 percent[8]. Life Insurance Funds comes second in terms of its share in the total growth of financial assets and reflects an upward trend, however, in terms of life-insurance penetration (measured as insurance premium income as a percentage of GDP), it remains abysmally low at 2.72 per cent, as on 2016 (Patnaik & Pandey, 2019). Similarly, Pension Funds’ assets[9] as a percentage of GDP stands at 1.05 percent, as on 2016 (Patnaik & Pandey, 2019).

Additionally, the share of retirement accounts such as pensions and provident funds and risk-mitigating products such as life insurance funds constitute a very small proportion of the overall household saving, potentially highlighting gaps in Indian households’ patterns of long-term savings and financial planning particularly for the retirement stage of their lives. Similar results were reported by the 2017 Household Finance Committee, which found that irrespective of the wealth of the households, retirement assets (such as PF and pensions) play a very limited role in households’ financial lives and there exists a prevalence of informal arrangements between parents and children to finance retirement. These results highlight the need for further penetration of formal financial services across a comprehensive suite of products given its links to economic growth and increased well-being[10].

Financial Liabilities

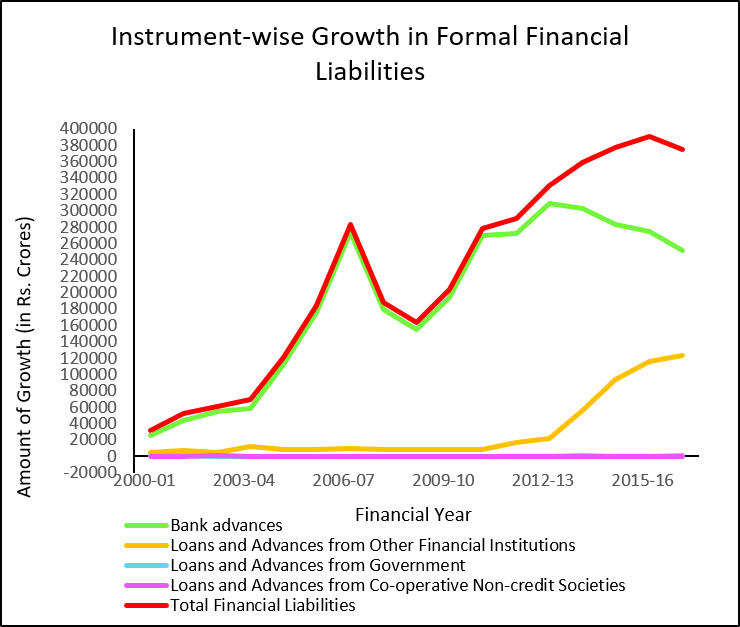

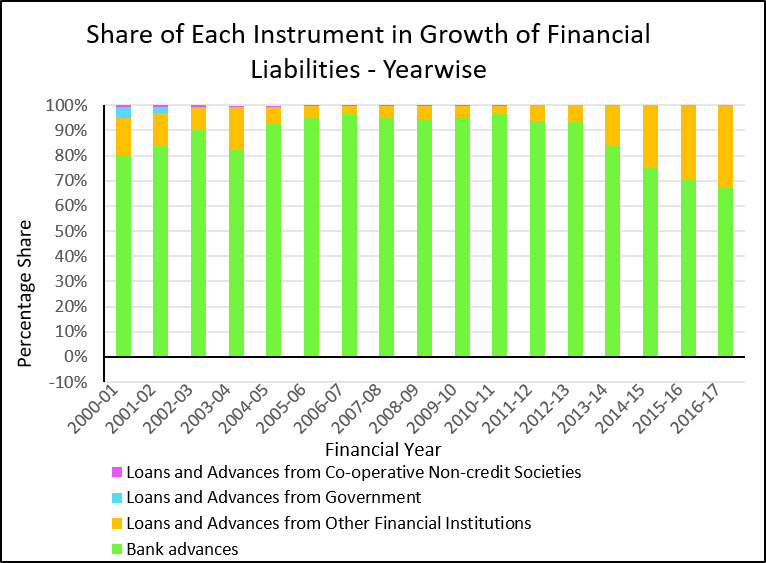

For the purpose of this blog, we restrict ourselves to the borrowing sources for the household sector as reported in the 2019 Annual Handbook of Statistics on Indian Economy. These include financial liabilities in the form of loans and borrowings from banks, housing finance companies and NBFCs (Reserve Bank of India, 2018). Graph 2A shows the growth in financial liabilities held by households across various instruments over the last two decades; Graph 2B captures the share of each instrument in the total growth of financial liabilities accrued by households, for each year in the analysis period.

Graph 2A: Instrument-wise growth in financial liabilities

Graph 2B: Share of each instrument in growth of financial liabilities

Financial liabilities accrued by Indian households grew consistently throughout the analysis period, at a CAGR of 12.6 per cent[11]. Loans and advances from commercial banks were the predominant drivers of this growth, contributing as much as 87 per cent on an average to the total growth in liabilities. While loans and advances from other non-bank institutions and co-operative non-credit societies contribute another 12 per cent, the rest is by loans and advances from the government. Interestingly, post the financial period of 2012-13, we observe a downward trend in bank loan and advances, which seems to correspond with an upward trend in loans and advances from other financial institutions, predominantly the NBFCs. With increasing levels of non-performing assets in the banking sector for the last five years, NBFCs seem to have substantially filled the credit gap in the market, as reflected in the above figures and overall sectoral trends[12]. Loans and advances from cooperative societies, on the other hand, is hovering around less than 1 per cent, given the structural, operational and viability challenges[13] with cooperatives and its declining agency in the financial sector.

Reviewing the growth in bank advances from a financial inclusion perspective, shows a less than optimal situation. As per the Inclusive Finance India Report 2018, the annual growth in the number of loan accounts and total outstanding loan for loans below Rs. 25,000 (largely catering to low-income segment), for the period 2012 to 2017, show recurring negative growth rates. Similarly, growth rates for credit both in terms of the number of accounts and total outstanding for priority sector lending, including small and marginal farmers and small businesses remain more or less static for the period 2012 to 2017. Therefore, even though the advances and loans from banks are the predominant drivers of financial liabilities, its implications for the low-income segment (based on secondary data available) in advancing access to credit seem negligible.

Although not reported here due to lack of data, micro-credit both through microfinance institutions and self-help group bank linkage programme have been extremely influential in expanding access to credit among low-income segment and constitute an important part of financial liabilities in Indian households’ financial portfolio.

Concluding Remarks

Overall, we see a consistent increase in the levels of household holdings across both financial assets and liabilities spanning roughly two decades, with growth in assets outpacing the growth of liabilities, leading to an increase in the financial net-worth of Indian households. While these are promising trends, the last decade has witnessed unprecedented efforts to accelerate access to formal financial services through newer types of financial institutions, innovative delivery channels, and rapid use of technology and there is resonance among sector stakeholders to focus increasingly on accelerating appropriate ‘usage’ of a comprehensive suite of formal financial products and services (including credit, savings and investment, insurance and retirement products) among Indian households.

It must also be noted that while this analysis is restricted only to formal financial market, Indian households largely save and allocate their wealth in physical assets. As per the Economic Survey 2019-20, for the year 2017-18, household savings in physical assets was equal to 10.3 per cent of GDP compared to savings in formal financial instruments equalling to 6.6 per cent of GDP. While the difference may not seem large, the share of physical assets in total household savings is significantly high at 60 per cent[14]. On the liabilities side, while there is continuous growth in financial liabilities accrued from formal institutions over the analysis period, we know from existing sources of research that unsecured debt primarily from non-institutional sources is the predominant source of debt; 56 percentage of Indian households were reported to have an outstanding debt from informal sources[15].

To summarise, the growth rates in financial instruments seem to be accompanied by a lack of adequate penetration across all types of products[16] highlighting significant gaps in the current state of formal financial market for the Indian household sector. While the availability of financial services has accelerated drastically in the last two decades, there is a need for financial deepening of existing products and services in order to enable households to ‘plan’, ‘grow’, ‘protect’ and ‘diversify’, optimally, for increased economic well-being.

__

Reference

Alok, M., & Ajay, T. (2018). Inclusive Finance India Report 2018. Access Publication.

Badarinza, C., Balasubramaniam, V., & Ramadorai, T. (2016). The Indian Household Savings Landscape. NCAER, India Policy Forum.

Campbell, J. Y. (2006). Household Finance. The Journal of The American Finance Association.

Ila, P., & Radhika, P. (2019). Saving and Capital Formation in India. NIPFP Working Paper Series.

Ramadorai, T. (2017). Report of the Household Finance Committee. New Delhi: Reserve Bank of India.

Reserve Bank of India. (2018). Quarterly Estimates of Households’ Financial Assets and Liabilities. New Delhi: Reserve Bank of India.

[1] The source for all the data used for the analyses and visualisations presented in the document is the RBI Handbook of Statistics on Indian Economy. For detailed explanations on the meanings of all financial instruments, other terminologies and potential limitations of the dataset, kindly visit the following link.

[2] For preparation of the estimates of domestic saving, the Central Statistical Organisation divides the economy into three broad institutional sector- private, public and household sector.

[3] The AIDIS-NSSO of the 70th round was used by the Household Finance Committee report to assess the state of Indian Household Finance.

[4] Relationship between Financial Depth and Economic Growth- https://dvararesearch.com/relationship-between-financial-depth-and-economic-growth/

[5] National Strategy for Financial Inclusion- https://rbidocs.rbi.org.in/rdocs/content/pdfs/NSFIREPORT100119.pdf

[6] Approximate calculation using the First Revised Estimates of 2016-17 and Quarterly Estimates of 2017-18 published by the Reserve Bank of India

[7] Data on currency holdings for the quarter post demonetisation can be found here- https://www.rbi.org.in/Scripts/BS_ViewBulletin.aspx?Id=17426

[8] India’s Findex Data and reasons for low usage- https://dvararesearch.com/2018/10/24/indias-findex-data-reasons-behind-non-usage-phenomenon-even-after-widespread-financial-services/

[9] Pension funds’ assets are defined as assets bought with the contributions to a pension plan

[10] Relationship between Financial Depth and Economic Growth- https://dvararesearch.com/2015/07/31/relationship-between-financial-depth-and-economic-growth/

[11] Approximate calculation using the First Revised Estimates of 2016-17 and Quarterly Estimates of 2017-18 published by the Reserve Bank of India

[12] https://www.theweek.in/news/biz-tech/2019/12/11/nbfc-assets-to-grow-at-decade-low-in-fy20-crisil.html

[13] Inclusive Finance India Report 2018- https://www.inclusivefinanceindia.org/uploads-inclusivefinance/publications/1065-1001-FILE.pdf

[14] Savings and Capital Formation in India- https://www.nipfp.org.in/media/medialibrary/2019/06/WP_271_2019.pdf

[15] https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/HFCRA28D0415E2144A009112DD314ECF5C07.PDF

[16] As substantiated by existing literature and data